Last week it was about the price of time, this week about what determines it at its core: Energy. Because markets do not evaluate the future in a vacuum. When energy becomes more expensive, scarcer or more uncertain, not only does the cost structure of the economy change, but also the foundation on which expectations, investments and ultimately bond yields rest. What appear to be separate spheres, energy here, financial markets there, actually turn out to be a single system. And it is precisely this system that is beginning to realign itself.

Last week, I argued that bonds are not merely financial instruments. They are the price of time. They tell us, quietly but relentlessly, what it costs to extend the present into the future. A mortgage depends on them. Corporate investment depends on them. Governments survive through them. When bond yields rise, the system is not only repricing debt. It is repricing duration, patience, confidence and, in the end, the future itself.

This week, it is worth returning to energy, because time is never priced in a vacuum.

As John Maynard Keynes once observed, markets are not governed only by arithmetic, but by expectations, by what we believe the future will look like. Energy, in that sense, is not merely an input. It is one of the foundations upon which those expectations rest.

One system, not two

The world likes to imagine that energy belongs to a separate conversation. Oil is for geopolitics, gas is for utilities, electricity is for engineers, and bonds are for central bankers and portfolio managers. This division is tidy, elegant and almost entirely false. The modern economy is not organised in such compartments. It is a single system of conversion and circulation. Energy makes production possible. Finance allows that production to be extended, anticipated and distributed through time. When one becomes unstable, the other does not remain untouched.

That is why the present tension in energy markets matters beyond the usual headlines. The public sees the obvious symptoms first: the price at the pump, the cost of heating, the irritation of another increase that arrives precisely when wages have not kept pace. But these are only the visible expressions of something more structural. An energy shock is never just a shock to fuel. It is a shock to expectations, to industrial costs, to freight, to chemicals, to food inputs, to confidence and, ultimately, to capital itself.

In that sense, the real issue is not whether the world is “running out” of energy. Apocalyptic language is emotionally satisfying, but economically lazy. Systems rarely collapse in a single theatrical gesture. They become less cheap, less fluid, less predictable. The damage begins at the margin. Transport takes longer. Insurance becomes dearer. Inventory buffers must be rebuilt. Industrial planning loses visibility. Governments rediscover subsidies. Central banks rediscover discomfort. The machine continues to run, but less gracefully than before and at a higher cost.

As Fernand Braudel would have reminded us, the decisive forces in economic history are rarely the visible shocks. They are the slow constraints that accumulate underneath.

The system, as it is

What is changing is not availability, but structure. And when one steps back from the rhetoric and looks at the system as it functions, the architecture becomes clearer and less reassuring.

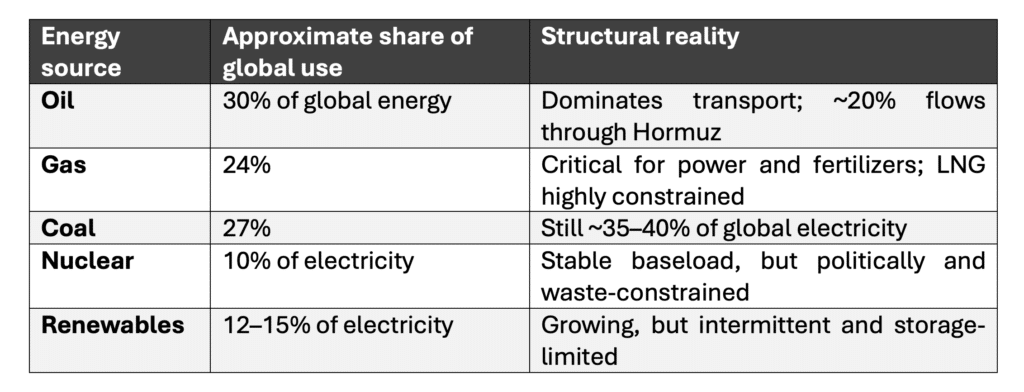

Roughly 100 million barrels of oil are consumed globally each day. Close to 20 per cent of that volume transits through the Strait of Hormuz, while another significant share passes through the Strait of Malacca. Liquefied natural gas follows a similar pattern, with Qatar alone accounting for around 20 per cent of global exports, much of it routed through the same vulnerable corridor. Coal still supplies roughly 35 to 40 per cent of world electricity generation, heavily concentrated in Asia. Nuclear provides stable baseload where deployed, while renewables, though growing, remain intermittent at roughly 12–15 per cent of global electricity.

Seen without illusion, the system reduces to the following:

This is not fragility in the dramatic sense. It is concentration. And concentration, when stressed, does not collapse. It reprices.

Or, as Thomas Schelling would frame it, vulnerability does not arise from weakness alone, but from tight dependencies in otherwise functional systems.

An asymmetrical world

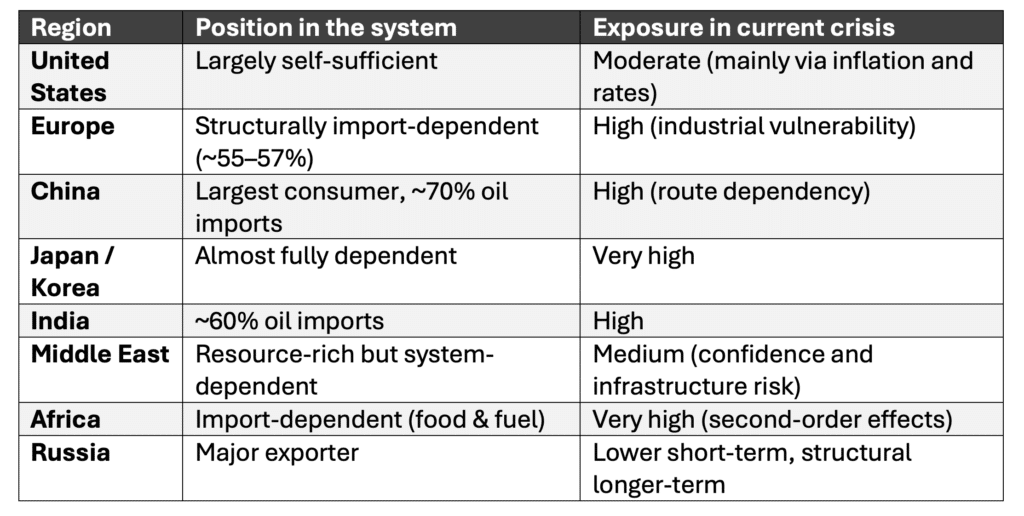

That structure translates directly into exposure across regions. Geography, in energy, is not incidental. It is structural.

“The current tensions around the Strait of Hormuz do not change this map. They reveal it.”

That higher cost matters because our economies were built, for several decades, on a deceptively generous assumption: that energy would remain abundant enough, transport smooth enough and money cheap enough for the whole architecture to keep expanding without confronting its physical limits too directly. Production could be fragmented across continents. Supply chains could be stretched to extraordinary lengths. Capital could remain optimistic because the system’s basic inputs appeared dependable. Cheap energy and cheap money did not solve every problem, but they concealed many of them. That concealment is becoming harder to maintain.

From energy to inflation

When energy insecurity returns, inflation ceases to be a technical variable and becomes again what it always was underneath the models: a physical phenomenon. If it costs more to extract, refine, insure, transport and transform what the economy needs to function, then the price structure of the whole system begins to shift. Not instantly, not uniformly, but unmistakably. One sees it first in freight, in fertilizers, in petrochemicals, in industrial margins, in the small humiliations of an economy whose complexity depends in fact on very basic things arriving where they must, on time and at tolerable cost.

From there, the matter enters finance.

Where the system is repriced

Bond markets are often described as though they belonged to a higher, more abstract plane, somewhere above the dust and steel of the real economy. In truth, they are simply where physical stress is translated into financial discipline. If energy makes inflation more persistent, central banks become less free to ease. If inflation expectations become less anchored, long-term yields become harder to compress. If long-term yields remain elevated, then the cost of time rises not only for governments, but for households, businesses and any institution whose survival depends on refinancing yesterday’s promises under tomorrow’s conditions.

This is where the connection with last week becomes more than rhetorical. When energy becomes less secure, time becomes more expensive.

The mechanism is not mysterious. It is almost vulgar in its simplicity. Dearer energy feeds costs. Higher costs complicate disinflation. More stubborn inflation limits monetary flexibility. Reduced monetary flexibility keeps yields higher than markets would otherwise prefer. Higher yields weaken balance sheets, restrain credit and expose every economic actor that had grown accustomed to a world in which time could be borrowed almost for free. The language may be financial, but the logic remains physical.

What makes the situation more uncomfortable is that this repricing of money is happening at precisely the wrong moment. For more than a decade, capital was abundant and cheap. If there was ever a window during which large-scale investments in energy infrastructure, storage, grid stability and industrial transition could have been financed with relative ease, that was it. Instead, much of that period was spent on financial engineering, asset inflation and, at times, symbolic commitments that were easier to announce than to implement.

Now the constraint is reversing. Capital is becoming more expensive at the very moment when the need for it is becoming more urgent. The transition, which requires scale, patience and massive upfront investment, is entering its most capital-intensive phase just as the price of time begins to rise again.

The uncomfortable truth is that the era of cheap money was not used to solve the problem, but to postpone it.

“And it is precisely at this point, when both energy and money cease to be cheap simultaneously that the intellectual confusion of the past two decades becomes most visible. Because what has often been presented as a question of policy, preference or even morality turns out, under pressure, to be a question of sequencing, discipline and physical constraints.”

A transition misunderstood

This is also why the usual political debate tends to miss the point. One camp speaks as though the transition away from fossil fuels were already well underway and merely needed a little more moral conviction. Another speaks as though hydrocarbons could be restored to their former innocence if only ideology stepped aside. Both positions flatter themselves. The first underestimates how deeply fossil energy remains embedded in industrial civilisation. The second underestimates how unstable and contested that dependence has become. We are not living after the age of oil and gas. We are living through the awkward and expensive phase in which societies claim to be leaving one energy system while continuing to rely heavily on it.

As Vaclav Smil has consistently argued, energy transitions are slow, capital-intensive and constrained by physics, not narratives.

Gas reminds us of this ambiguity. It is fashionable to speak of it as a transition fuel, which is another way of admitting that the bridge has not yet been crossed. Electricity may be the desired destination, but electricity still requires continuous generation, stable grids and storage capacities that remain, despite much piety and many subsidies, less miraculous in practice than in conference language. When the wind drops and the sun is absent, economies become rapidly less philosophical. They return to what works. Often that means gas. Sometimes, humiliatingly, it means coal. Reality has a way of embarrassing doctrine.

The discipline of trade-offs

We have been here before. The oil shocks of the 1970s exposed raw dependence on imported energy and forced a reckoning with physical limits. France responded with a clear-eyed strategic decision: it launched a massive nuclear build-out, rapidly constructing dozens of standardized reactors. The bet was pragmatic, not ideological. Faced with vulnerability, France chose a dispatchable, high-density source capable of delivering stable baseload power and reducing reliance on volatile imports. Today nuclear still accounts for roughly 65–70 per cent of French electricity.

Contrast that long-horizon discipline with more recent choices in parts of Europe. Wind farms were built. Solar capacity expanded. But at the same time — more discreetly, almost quietly — gas-fired power plants were also constructed, precisely because engineers knew that intermittency cannot sustain an industrial system on its own. The paradox is not hidden. It is structural. We built intermittent systems and, in parallel, ensured that something reliable would still carry the load when reality intervened.

The problem is not that renewables were developed. The problem is that the system was never fully thought through.

“Storage, the only true solution to intermittency, remained the missing link.”

As Friedrich Hayek warned, the illusion that complex systems can be engineered through intent alone, without respecting dispersed knowledge and constraints, is often the most dangerous mistake of all.

Storage: the missing link

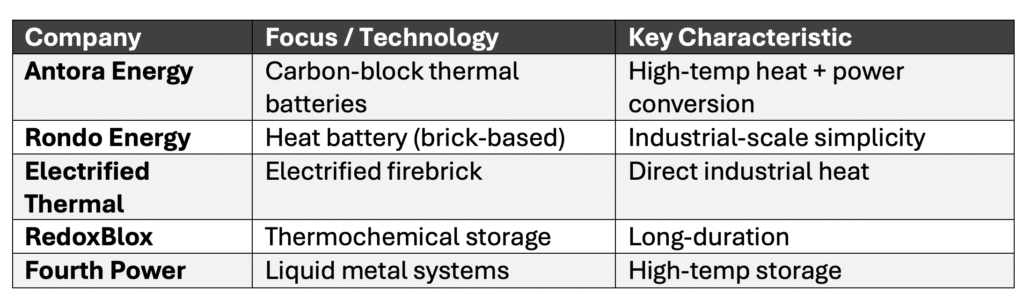

It is therefore striking, and somewhat ironic that the country with the most abundant and diverse energy resources, the United States, is currently showing one of the more pragmatic paths forward on the storage challenge for industrial applications. Companies such as Antora Energy are scaling thermal batteries that store surplus electricity as high-temperature heat in abundant, low-cost materials like solid carbon blocks. These systems then deliver reliable industrial heat or convert it back to power on demand.

Several US competitors are advancing similar approaches:

China, meanwhile, is scaling massively both CSP (concentrated solar power) with molten salt storage and traditional batteries. Europe, by contrast, risks falling between ambition and execution, strong in targets, less decisive in system integration.

The quiet shift

None of this means that catastrophe is inevitable. It means something more sober and perhaps more serious: adjustment is unavoidable. The countries best positioned will not be those with the best narratives. They will be those with redundancy, resources and discipline.

Africa, often absent from strategic discussions, remains the most exposed. Not because of direct energy dependency alone, but because energy transmits into food, and food into stability. When energy rises, food follows. And when food follows, adjustment ceases to be theoretical.

Conclusion: equilibrium returns

Energy shocks do not end systems. They reveal them. For years, advanced economies cultivated the illusion that value had become weightless. Yet nothing fundamental has changed. Steel still needs heat. Fertilizer still needs gas. Transport still needs fuel. Data still needs electricity.

Bonds tell us what it costs to sustain a promise. Energy tells us what it costs to sustain a civilisation. When both are repriced, the message is not collapse. It is constraint.

For years, money concealed those limits. Now energy is revealing them. The system will not break. It will simply become more honest. A new equilibrium will emerge, not because it was designed, but because it becomes unavoidable.

As Albert Hirschman wrote, progress often comes not from perfect planning, but from the pressures that force systems to adjust. This is one of those moments.

And this time, the bill is being presented in energy and paid in time.

Time, it turns out, was never free. It was simply underpriced.

Eric Lefebvre

Read also: The system runs on blood

Search:

Sponsors: