The global financial system appears abstract, but at its core it functions like an organism: it thrives on flow. Not just from energy, but from credit, expectations and time. In the past, when money was virtually free for a long time, this cycle was able to expand seemingly without a hitch. But with rising interest rates, geopolitical tensions and a creeping shift in the global flow of capital, something fundamental is beginning to change.

Last week’s column began with the topic of energy, and for good reason. Leaving aside the language of institutions, politics and markets, economic power is still based on something thoroughly physical: the ability to mobilize energy and convert it into power. This is the basic prerequisite. Without energy there is no production and without production there is no economy worth describing.

But production alone is not enough. A system may have resources, infrastructure and industrial capacity, but still falter when something essential stops flowing through it. Economies are like living organisms and depend on more than just inputs. They depend on circulation. They need a continuous flow that connects current activities with future promises, current needs with deferred payments and production with purchasing power.

In modern economies, this flow is organized through loans. And loans are organized on a large scale through bonds.

The word itself may sound technical, even abstract, but the instrument is simple enough. A bond is a promise stretched out over time: One party lends money, another agrees to repay it, with interest. But this interest is more than just compensation for patience or risk. It is the price that is set on time itself, and few prices in the modern system are of greater importance.

It is important because it is quietly behind almost everything. Mortgage interest rates result from it. Corporate investments are filtered through it. Governments finance themselves through it. Even stock market valuations, for all their apparent independence, are tied to it through discount rates and expectations. You could almost say that if energy remains the hidden engine of the real economy, then bonds have become the invisible architecture of its financial cycle.

For much of the period after the global financial crisis, this architecture seemed unusually forgiving. Central banks kept interest rates close to zero, bought huge amounts of bonds and made time cheap. The system adapted to these conditions with remarkable speed. Debt grew, valuations rose, and what had once been an emergency measure slowly came to resemble the natural order of things.

That is the illusion that is now beginning to fade.

The recent development of yields on US government bonds, particularly 10-year bonds, should be viewed against this backdrop. A yield of around 4.4 percent may not sound dramatic to the uninitiated. However, in a market of this size and after a decade characterized by extremely cheap money, this is not an insignificant fluctuation. It is a re-evaluation of time, and when time is re-evaluated, much else in the system follows.

A market of global proportions

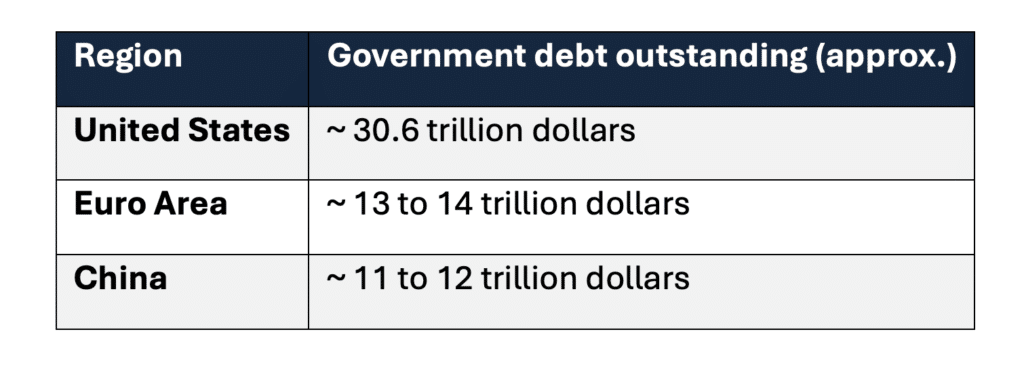

To understand the significance of this revaluation, it is important to consider the scale of the market in which it is taking place. The US government bond market, with an outstanding market volume of around 30.6 trillion dollars (as at the beginning of 2026), is not only large. It is the central point of reference for the global financial world. Its size exceeds that of any other government bond market, and its yields serve as a benchmark far beyond the borders of the USA.

A simple comparison illustrates the asymmetry.

This is not just a difference in size. It reflects a difference in function. The US market absorbs global capital, forms the base against which other assets are valued, and requires continuous demand to maintain its size. For decades, this demand was supported by a structure that extended beyond the financial sector.

The cycle that financed the system

Since the 1970s, most global energy trade has been conducted in dollars. Countries that needed oil needed dollars, countries that exported oil accumulated them. These dollars were in turn reinvested, primarily in US financial assets and above all in government bonds.

This process, often referred to as “petrodollar recycling”, was not based on formal agreements. It continued because it aligned incentives. Energy created demand for dollars. Dollars created demand for bonds. Bonds financed the system.

The cycle was not perfect, but stable enough to maintain a certain configuration of the global financial world. Even today, around 80 percent of global oil transactions are still based on the dollar. But the structure is loosening at the edges. Large energy transactions are increasingly being settled in yuan, the BRICS+ countries are expanding settlement mechanisms outside the dollar system, and the dollar’s share of global foreign exchange reserves has fallen from around 71 percent in 2000 to around 56 to 59 percent today.

Central banks have responded by diversifying. They bought record amounts of gold in 2025 and continued to do so at a similar pace into 2026, led by emerging market reserve managers looking for assets that are independent of redemption promises.

The consequence is subtle but significant. Lower automatic demand for US Treasuries is contributing to higher long-term yields, tighter financial conditions and a gradual shift towards a more multipolar reserve system. The recent disruptions in the Strait of Hormuz have only exacerbated this dynamic, as energy uncertainty is fueling both inflation and reserve diversification.

The shift is still incomplete. But systems rarely change abruptly. They first move at the edges before they change at the core.

When prices move, the balance sheets follow

The bond market is often perceived as abstract. In reality, the way it works is simple. A bond issued in the past offers a fixed yield. When interest rates rise, new bonds offer higher yields. The existing bond does not change, but its relative attractiveness does. Its price adjusts downwards.

This is not a question of mood. It is pure arithmetic. A useful way to understand this mechanism is to follow its sequence. When yields rise, bond prices fall. When bond prices fall, the value of existing portfolios falls. When portfolios lose value, balance sheets weaken. When balance sheets weaken, lending capacity tightens. And when lending capacity tightens, economic activity slows.

This chain rarely unfolds all at once. But it unfolds with remarkable regularity.

A rough rule of thumb illustrates the extent of this. An increase in yields of one percentage point can reduce the price of a typical ten-year bond by around 7 to 9 percent, depending on its maturity. In a market worth tens of trillions, such adjustments are not marginal.

Banks, insurers and pension funds hold large portfolios of these assets. A rapid rise in yields reduces the market value of these portfolios. The effect is often gradual, sometimes disguised by accounting rules, but it leads to tensions that can become visible under stress.

This mechanism has been observed repeatedly.

During the European sovereign debt crisis in 2012, the restructuring of Greek government bonds led to losses of over 50 percent for private investors. Institutions that had regarded government bonds as stable investments suddenly found themselves exposed to risks. Among them, Groupama recorded significant losses as the value of its holdings fell sharply.

More recently, in 2023, US regional banks such as Silicon Valley Bank faced significant unrealized losses on long-duration bonds as interest rates rose rapidly. These losses became critical when deposit outflows forced the sale of assets. In 2022, UK pension funds pursuing liability-driven investment strategies were similarly destabilized by sharp increases in yields, triggering margin calls and forced close-outs.

In each case, the pattern was the same. The bond market did not absorb the shock. It passed it on.

A system under tension

The current environment reflects a different constellation, but one that brings its own form of tension. Economic growth is showing signs of weakening. The labor market data has softened. But the escalation in the Middle East, with US and Israeli attacks on Iran from the end of February 2026 and the subsequent disruption in the Strait of Hormuz, has triggered a major energy shock. Oil prices have skyrocketed, with Brent crude well over USD 100 per barrel.

This leads to a difficult balance. Lower growth would normally justify lower interest rates. Sustained inflation requires the opposite. The system is therefore pulled in two directions at the same time.

Inflation expectations have risen sharply. The OECD is now forecasting overall inflation in the US of 4.2% for 2026. This represents a significant upward correction driven by the energy shock. The result is a familiar scenario: higher prices with a simultaneous decline in growth, similar to the oil-driven phases of the 1970s.

In Europe, the impact is immediate and visible. Diesel prices have risen to 2 euros per liter or more in several countries, which has a direct impact on transport costs, food prices and industry margins.

The bond market does not resolve this contradiction. It reflects it.

The signal within the curve

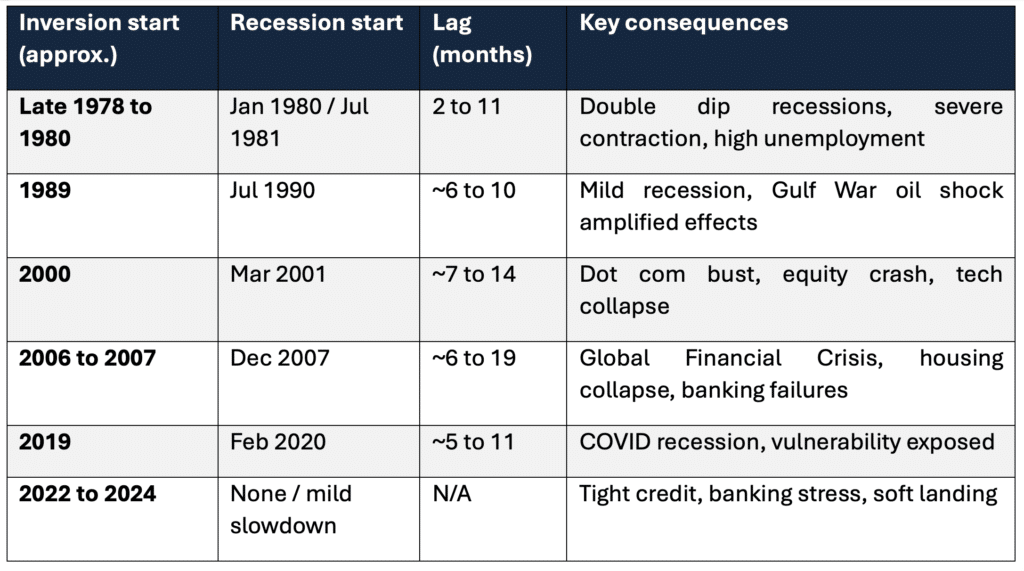

One of the clearest ways in which this tension becomes visible is in the shape of the yield curve, i.e. the relationship between bond yields and their maturities. Under normal conditions, longer maturities offer higher yields. Time brings uncertainty, and this uncertainty requires compensation.

However, there are times when this relationship is reversed. Short-term interest rates exceed long-term interest rates. The curve inverts. This inversion is not just of a technical nature. Its significance is immediate and historically significant.

It implies that the markets are assuming that the current tense financial conditions will ease in the future. Investors are pricing in an economic slowdown or recession and expect central banks to eventually cut interest rates. Long-term yields fall as they reflect lower expected growth and lower inflation in the future.

Historically, this has been one of the most reliable early indicators of a recession.

The table is important because it captures something deeper than a statistical regularity. The yield curve does not predict events in a mechanical sense. It signals that it is becoming increasingly difficult for the system to maintain the current price of money.

Normalization of the yield curve today

The record-long inversion that began in 2022 ended in late 2024 or early 2025. By March 2026, the curve had returned to a normal upward slope. The 2-year yield is just under 4% and the 10-year yield is just under 4.4%, resulting in a positive spread of around half a percentage point.

This steepening reflects a double move. At the short end, the markets continue to expect a later easing. At the long end, yields remain under pressure from high issuance, fiscal concerns and the renewed energy shock.

Normalization does not eliminate risks in this context. It marks a transition. The most acute warning is over, but the time costs remain high. The system has picked up the signal. But not without consequences.

A simple conclusion

What emerges from all this is not a forecast of imminent collapse, but a change in the framework conditions. For a long time, energy was plentiful and money was so cheap that the system was able to expand without directly reaching its limits. This constellation no longer fully exists.

Energy has become less predictable. Money has a price again. None of these changes is decisive on its own. Together they change the balance of the system.

The bond markets do not simply reflect these changes. They pass them on. They determine how easily the future can be financed, how easily existing obligations can be met and how far the system can expand before an adjustment becomes unavoidable.

The economy will not come to a standstill. It will adapt, as it always does. But adaptation in this context means operating under stricter constraints, where the cost of time once again plays a role.

And when the cost of time plays a role, what was previously invisible tends to reappear. Not suddenly. But unmistakably.

When money was free, the system expanded. When money has a price, the system reveals its limits.

Eric Lefebvre

Read also: The driving forces of power

Search:

Sponsors: