Money is more than just a means of payment: it is the medium with which the future is financed. When energy becomes scarce, inflation persistent and trust fragile, it is precisely this system that comes under pressure.

Last week I argued that bonds are not just financial instruments. They are the price of time itself, the quiet meter that tells us what society is willing to pay to stretch the present into the future. A mortgage, a corporate expansion, a government’s survival: all of them rest on that price. When bond yields rise, we are not merely repricing debt. We are repricing patience, confidence, and ultimately the future itself.

This week, we go one layer deeper.

If bonds price time, then money is the medium through which time is bought and sold. And right now, that medium is beginning to lose something essential, not its function, not its liquidity, but its reliability.

We like to imagine that the economy can be decomposed into separate conversations. Energy belongs to geopolitics. Inflation belongs to economists. Central banks belong to finance. Each domain has its vocabulary, its specialists, its reassuring boundaries. It gives the impression of order. But that order is artificial.

The modern economy is a single system of conversion and circulation. Energy makes production physically possible. Money allows that production to be anticipated, financed, and extended across time. Expectations, those fragile, invisible structures on which markets depend, rest on both. When one becomes unstable, the other cannot remain untouched. There is no separation, only interaction.

The quiet misunderstanding: what inflation actually is

We are often given explanations for inflation that are politically convenient and intellectually incomplete. Prices rise, we are told, because companies are greedy, or because wages are rising too fast, or because consumers are spending too freely. These narratives are attractive because they assign responsibility in human terms.

But they miss the underlying mechanism. Inflation is not primarily a story about prices. It is a story about money.

Imagine ten apples and ten coins. Each apple costs one coin. Now imagine that the number of apples stays the same, but the number of coins doubles. There are still ten apples, but now twenty coins are trying to buy them. The apples have not changed. The money has. Prices must adjust. That is not ideology. It is basic accounting.

Wages and corporate margins can redistribute inflation. They do not create the excess purchasing power in the first place. Only the expansion of money does.

For most of modern history, money was constrained by something outside the system. Under the gold standard, currencies were linked, at least in principle, to a physical anchor. The quantity of money could not expand indefinitely without reference to a limited resource.

That constraint no longer exists. Today’s currencies are fiat currencies. They are not backed by gold. They are backed by trust, by institutions, by central banks, and by the expectation that their value will remain broadly stable. This gives flexibility. It also removes discipline. Because if money can be created when needed, it often will be.

The plumbing: what M1 and M2 actually mean

To understand what is happening today, one has to look beyond interest rates and into the quantity of money itself.

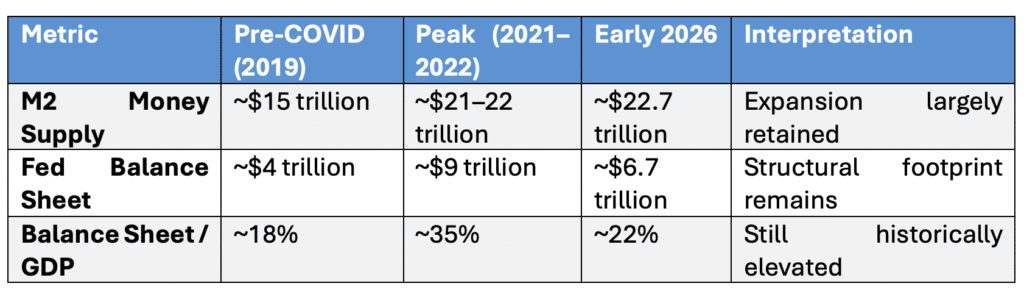

M1 represents immediately spendable money: cash and deposits that can be used for transactions right away. M2 is broader. It includes M1 plus savings deposits and other near-money assets that can quickly become spending power. These measures are not abstract constructs. They describe the stock of purchasing power circulating in the system, the fuel that drives demand.

During the pandemic, that stock expanded at a pace rarely seen outside of wartime. The Federal Reserve’s balance sheet ballooned, and broad money supply surged accordingly. Even after some reversal, the system has not returned to its previous configuration.

Seen this way, the numbers stop being technical and start becoming structural. They describe a system in which the quantity of monetary claims has increased far more rapidly than the underlying productive base.

This was sold as emergency medicine. In many ways it was. But emergency money does not evaporate when the crisis fades. It lingers. It circulates. It accumulates claims on a real economy that cannot grow fast enough to absorb it all.

What we are living through now is not simply the result of current policy or current shocks. It is the delayed consequence of yesterday’s expansion.

Inflation is not an accident. It is the bill coming due.

Energy returns as the hard constraint

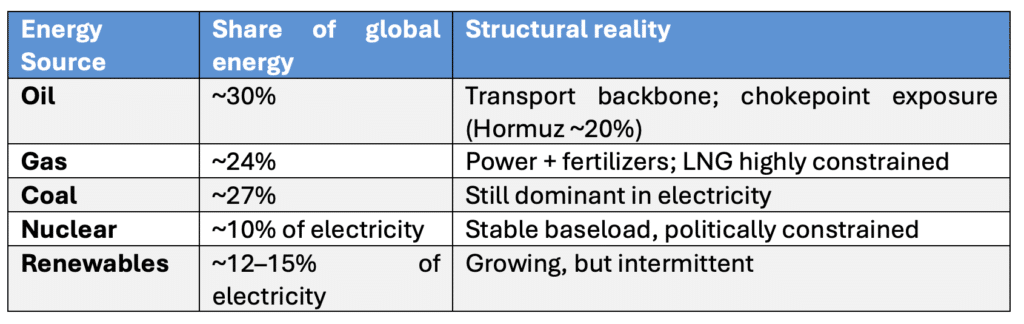

If the story stopped there, the adjustment might have remained manageable. But it does not stop there. Because money does not operate in a vacuum. It operates within a physical system, and that system has limits.

Global energy flows remain concentrated and, under stress, surprisingly rigid. Oil, gas and electricity are not interchangeable abstractions; they are physical processes constrained by infrastructure, geography and time. When those constraints tighten, the entire economic structure feels it almost immediately.

Recent tensions around Iran, and the renewed focus on key chokepoints, have once again pushed oil prices higher. That increase does not remain confined to energy markets. It moves through transport, through production, through food.

And at that point, the monetary and the physical collide. The system is carrying more purchasing power than before. At the same time, the real capacity of the system is becoming more constrained, more expensive, less predictable.

This is no longer ordinary inflation. It is compounded inflation, monetary expansion meeting physical limits.

The central bank trap

It is within this configuration that central banks now operate.

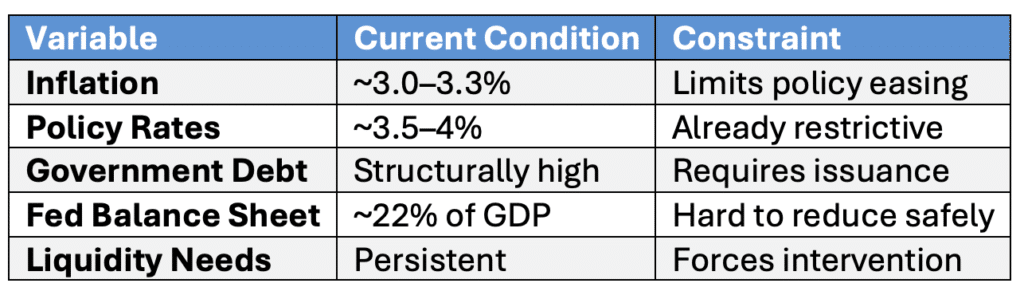

They face inflation that remains above target. They face economies built on large and growing debt. They face governments that must continue issuing bonds at scale. And they face financial systems that have become dependent on liquidity.

The constraints can be summarised simply, though they are anything but simple in practice:

The Federal Reserve has already adjusted, though without dramatic announcements. Quantitative tightening has effectively ended. Balance sheet expansion has resumed under softer language. Liquidity is being added even as inflation refuses to return cleanly to target.

This creates a situation in which policy is pulled in two directions at once. On the one hand, inflation demands restraint. On the other, the structure of the system demands support.

What emerges is not a clear strategy, but a managed contradiction, a central bank attempting to stabilize a system whose internal tensions are no longer easily reconciled.

The wrong moment

What makes this moment particularly uncomfortable is not just the configuration, but the timing. For more than a decade, money was cheap. That was the moment when long-term investment in energy systems, grids, storage and resilience could have been financed with relative ease.

That moment has passed. Now the cost of time is rising precisely when the system requires massive new investment to address its vulnerabilities. The transition in energy, which is not ideological but physical, is entering its most capital-intensive phase just as capital itself becomes more expensive.

Cheap money did not solve the problem. It postponed it. And postponed problems rarely return in a more convenient form.

History’s warning, and the present variation

We have seen versions of this dynamic before.

In the 1970s, inflation did not emerge suddenly. It accumulated, slowly at first, then more visibly. Policymakers hesitated, constrained not by ignorance but by politics. The cost of decisive action, higher unemployment, lower growth, was too immediate, too visible, too difficult.

When Paul Volcker finally acted, the adjustment was brutal. The system had to be forced back into balance.

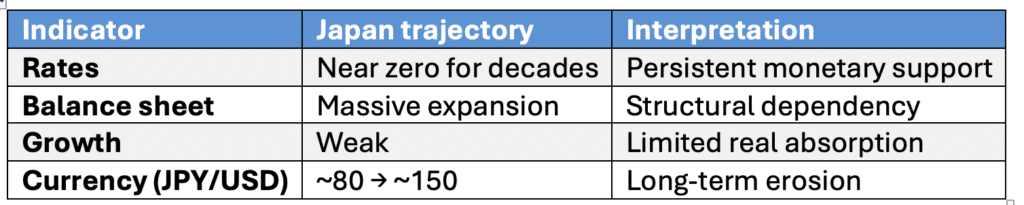

Inflation, once embedded, does not retreat voluntarily. Japan offers a different, more gradual illustration of the same tension.

Not collapse. But a slow loss of purchasing power in a system where money expanded faster than reality.

The eurozone: a different fracture

The eurozone adds another layer of complexity, and perhaps a more immediate one. The euro is a monetary union without a true fiscal union. It binds together economies with different structures, different growth profiles, and different debt dynamics under a single currency and a single monetary policy.

That arrangement works in stable times. It becomes fragile under stress.

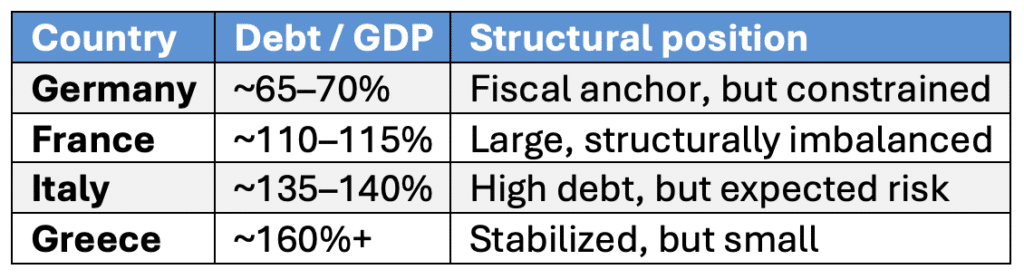

What is now emerging is not a replay of the Greek crisis, but something potentially more difficult to resolve. Greece was small enough to be stabilized through external support. France is not. France has become, in many respects, the weak link, not because of sudden collapse, but because of accumulated structural imbalances: high public spending, persistent deficits, rising debt levels.

The difficulty is not simply that France is weakening. It is that Germany, which historically provided the stabilizing force within the system, no longer has the same capacity, politically or economically, to underwrite the entire structure.

This creates a tension that is more subtle, but potentially more dangerous, than previous crises. The system cannot easily fragment. But it cannot easily converge either. Under those conditions, monetary policy becomes the balancing mechanism of last resort.

And monetary policy, when used to hold together structurally divergent systems, tends to drift toward accommodation.

The bond market’s verdict

The bond market is already expressing its discomfort, though not always in dramatic fashion. Long-term yields remain elevated, reflecting a growing hesitation to assume that inflation will return smoothly to target without further disruption. This is not a market in panic. It is a market reassessing.

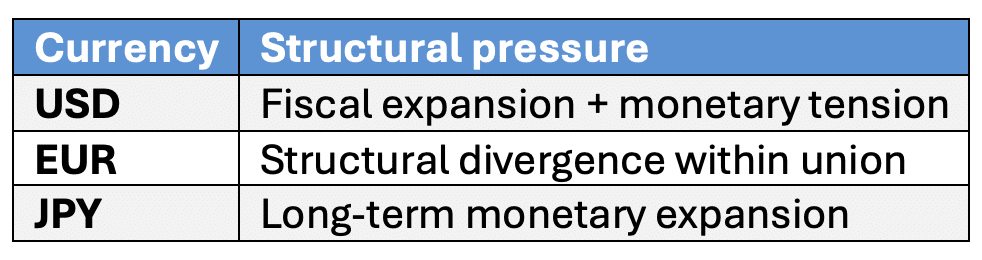

Currencies tell a similar story.

Each reflects a different version of the same question: how stable is money when the system that supports it is under strain?

Money under pressure

For a generation, money was treated as neutral, stable enough to disappear into the background. That assumption is now being tested.

Not abruptly, but persistently. The constraints are becoming visible again. Energy is no longer cheap and predictable. Time is no longer free. And trust, the invisible foundation of fiat money, is no longer entirely unquestioned.

The system is not collapsing. But it is being forced into a more honest equilibrium.

Money, in that process, becomes the variable through which the adjustment takes place. Not through sudden failure, but through gradual repricing, through shifts in purchasing power, in expectations, in what it costs to carry value across time.

And that leads to a final observation. Money was never truly anchored by institutions alone. It was anchored by belief, the belief that tomorrow would resemble today closely enough for promises to hold. That belief is beginning to change.

And when money begins to reprice time under those conditions, the consequence is not simply higher inflation or higher yields. It is a future that becomes more expensive to finance, more uncertain to plan, and ultimately less predictable to inhabit.

What follows from here

What follows from this is not a forecast in the conventional sense. It is not a question of whether rates will move by twenty-five basis points more or less, or whether the next quarter will surprise to the upside or the downside. Those are surface movements.

What matters is that the range of possible outcomes is narrowing.

The system is no longer free to choose its path without consequence. Too much money has already been created to return effortlessly to a world of stable prices. Too much debt has accumulated to tolerate high interest rates for long without destabilising the structure that depends on them. And too little has been invested, in the years when capital was cheap, to make the physical adjustment painless.

Under those conditions, the future does not branch into infinite possibilities. It compresses into a small number of paths, each with its own cost.

One path is discipline. Monetary policy remains tight, liquidity is withdrawn, and inflation is forced back toward target through restraint. This is the path associated with Paul Volcker, the path that restores credibility by imposing it. But it comes with immediate and visible consequences: weaker growth, financial stress, rising unemployment, and political resistance. It is effective, but it is rarely chosen early, because the cost is too evident and too concentrated.

Another path is erosion. Inflation is not defeated, but managed. It remains slightly above target, not dramatically, not catastrophically, but persistently. Nominal growth carries the debt. The system adjusts not through crisis, but through gradual dilution. In such a world, money continues to function, but its ability to preserve value weakens over time. This path is less visible, less abrupt, and therefore more politically acceptable. It is also the path toward which systems tend to drift when the alternative becomes too painful.

A third path exists in theory, though it rarely remains stable in practice. Policy oscillates. Central banks tighten when inflation rises, then ease when the system begins to strain. Each cycle avoids immediate rupture, but at the cost of coherence. Over time, that inconsistency erodes confidence, and the system becomes more reactive, more fragile, more dependent on intervention.

We are not fully in any one of these paths. But we are no longer in a world where none of them apply.

The direction of travel

If one looks not at intentions, but at constraints, the direction becomes clearer. A system characterised by structurally high debt, political limits on austerity, and a central bank already returning, quietly, to balance sheet expansion is unlikely to sustain prolonged monetary discipline. The theoretical option remains, but the practical capacity to execute it weakens with each cycle.

What is more likely is not collapse, but drift. Not toward crisis, but toward a form of managed erosion.

Inflation that is contained but not eliminated. Interest rates that are elevated, but not sufficiently high in real terms to fully restore monetary stability. A system in which the burden of adjustment is carried less by abrupt correction than by gradual dilution.

In other words, a world in which the cost of holding value increases quietly over time.

The implication

In such a world, the adjustment does not arrive as a shock. It unfolds slowly. Money continues to circulate, but it does not behave in the same way. Cash ceases to be neutral. Long-duration promises become more fragile. The difference between nominal and real value becomes more consequential.

What changes is not only the level of prices, but the reliability of the unit in which those prices are expressed. The shift is subtle, but profound. It is not a transition from stability to instability. It is a transition from assumed stability to conditional stability.

The closing loop

And that brings us back to where we began. Bonds price time. Money makes that pricing possible. But when money itself begins to lose reliability, the entire structure is affected. Time becomes harder to extend. Promises become harder to value. The future becomes more expensive to finance.

The system will not break. It will adjust. But it will adjust in a way that forces a recognition that had been postponed for a long time: that neither money nor energy was ever infinite, and that when both are repriced at once, the illusion of abundance disappears with them.

For years, money concealed those limits. Now it is revealing them. And in that process, something else becomes visible, something that is rarely stated plainly. Inflation is not only a rise in prices. It is a transfer.

It is a transfer from those who hold money to those who issue it. From savers to borrowers. From the past to the present.

When money loses purchasing power, nothing disappears. Value is redistributed. Quietly, continuously, without a vote and without a line item in any budget.

In that sense, inflation is a form of taxation not legislated, not debated, but embedded in the structure of the system itself. It is the most discreet form of taxation, because it does not arrive as a bill. It arrives as a gradual erosion. A loss that is felt but rarely traced back to its source.

And this is where the current moment becomes more than a cyclical adjustment. Because a system that carries high levels of debt, that depends on continuous refinancing, and that cannot easily impose austerity, has a natural inclination toward this form of adjustment. Not because it is designed that way explicitly, but because the alternatives are more immediate, more visible, and more politically difficult.

So, the burden shifts. Not through crisis, but through dilution. Not through default, but through time. And that is perhaps the most important implication of all. When money reprices time under these conditions, the question is no longer simply how expensive the future becomes. It is who, quietly, is paying for it.

Eric Lefebvre

Read also: When energy reassesses time

Search:

Sponsors: