The 2026 IVW Annual Conference at the Kunsthaus Zürich focused on an uncomfortable question: Does the insurance industry still live up to its core promise of making the unforeseen manageable? The answer was nuanced. And uncomfortable.

It was no coincidence that the annual conference of the Institute for Insurance Economics (ISG-HSG) was once again held at an unconventional venue. “The Other Conference,” as the self-chosen motto goes, deliberately seeks out settings that invite reflection and take participants away from the daily grind. The lecture hall at the Kunsthaus Zürich proved to be a suitable setting for a discussion that delved deeply into systemic issues facing the industry: Where does the market fail? Where should the government step in? And what can insurers do on their own?

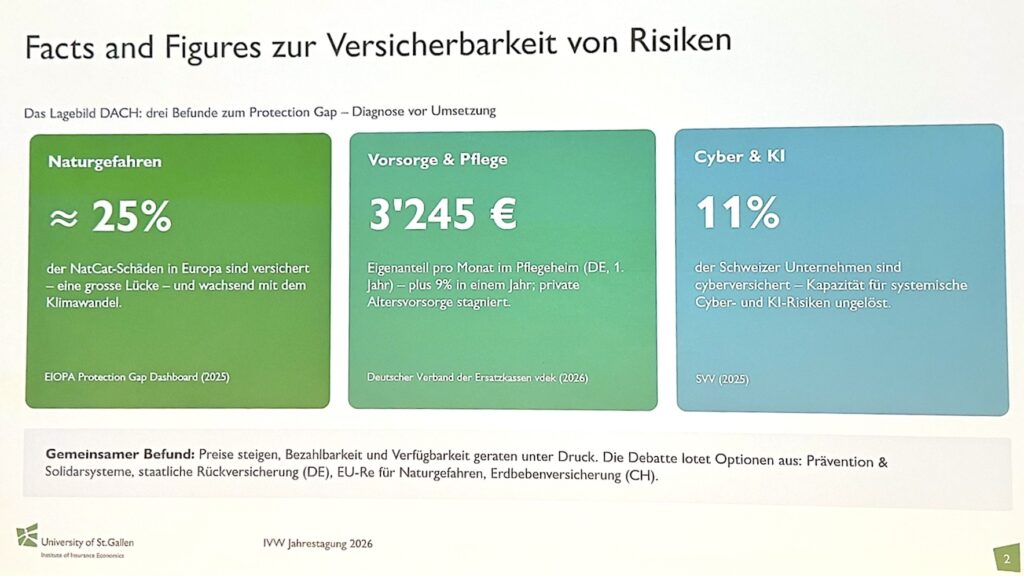

25 percent: a sobering figure

The session began with three figures that sharply highlighted the conference theme, “Protection Gap.” Only 25 percent of the damage caused by natural disasters in Europe is insured. The rest falls on citizens, businesses, and public budgets without any financial buffer. Carlos Giuné, Head of Sustainability at EIOPA, the European Insurance and Occupational Pensions Authority, explained via video link from Frankfurt that this gap is not stagnating but is growing. And it hits hardest those who already have the fewest resources to protect themselves.

Guiné referred to the EIOPA dashboard on natural hazard coverage, which has been providing country-specific comparative figures for EU member states since 2022 and has, at the very least, raised awareness. Several European countries, including Italy, Greece, and Portugal, have since launched debates on mandatory coverage models. Germany is engaged in lively discussion. By Swiss standards, this sounds familiar.

On the demand side, EIOPA identified several drivers of underinsurance: a lack of risk awareness, the expectation of government compensation in the event of a loss, and a lack of trust in the insurance industry. The concept of “impact underwriting”—under which insurance policies are designed to actively reward preventive behavior—was proposed as a possible approach, but Nicolas Jeanmart of Insurance Europe expressed a pragmatic reservation: the financial incentives for individuals are often simply too small in relation to the investment costs.

DACH: Three Countries, Three Stages of Development

The panel discussion that followed laid bare the differences within the German-speaking world. Austria is grappling with a political obstacle, which Christian Eltner of the Austrian Insurance Association described succinctly: As long as the government steps in with disaster relief funds after flooding events—and the distribution of those funds varies depending on the timing of elections—there is no pressure to develop a private-sector insurance solution. The model is economically dysfunctional, but politically difficult to dismantle.

Germany is a step ahead. There is a proposal for mandatory insurance against natural hazards, which is enshrined in the government’s platform. However, actuary Monika Sebold-Bender (Marco International Insurance) pointed out that a flat premium creates the wrong incentive: Prevention and personal responsibility would be undermined if the risk were leveled out through pricing. The right solution, she argued, is risk-based pricing with social compensation provided through government funds—not through the insurance industry’s own pricing mechanism.

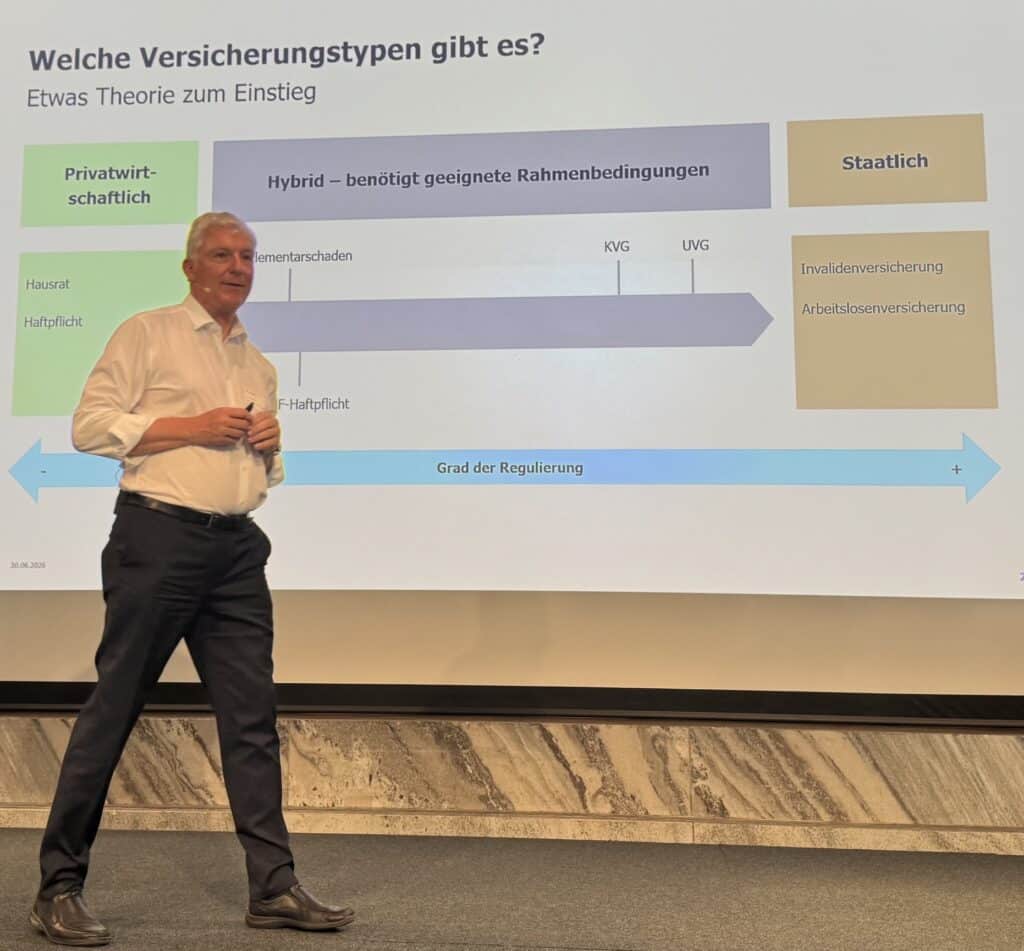

Switzerland has largely resolved the issue of natural disaster insurance through mandatory coverage in 22 of 26 cantons and high penetration rates in the remaining cantons. One gap remains: earthquakes. Dr. Lukas Summermatter, Director of the St. Gallen Cantonal Building Insurance, and Prof. Dr. Hato Schmeiser of the IVW-HSG agreed that the risk is, in principle, insurable. The main problem is not capacity, but awareness.

Cyber: An 89 Percent Growth Market

Urs Arbter, director of the Swiss Insurance Association (SVV), shared what was arguably the most striking statistic of the afternoon: 89 percent of Swiss SMEs do not have cyber insurance. According to Arbter—who put a deliberately positive spin on it—this is not a disaster, but rather a growth market. Demand arises only where risks exist. Only where new risks emerge is there potential for growth.

The workshop session on cybersecurity and AI provided further insight. On the supply side, the issue isn’t a lack of products, but a lack of accessibility. A five-person craft business can hardly meet patch management requirements. What it needs is an action plan for emergencies and an insurer willing to support the business—not just insure it. The term “Protection as a Service” came up several times.

Samuel Staubli of Zurich Insurance highlighted ten key controls that were identified in collaboration with the industry and are intended to provide comprehensive risk coverage. Digital tools, AI-powered risk analyses, and embedded insurance solutions—such as the platform developed in collaboration with UBS—show that the market is on the move. But the steps taken so far remain small compared to the potential.

Systemic cyber risk—that is, the cumulative damage that occurs when an attack paralyzes an entire infrastructure—remains the core problem that is difficult to solve. The consensus is that, without public-private partnerships, the private sector alone cannot bear this risk in the long term.

Long-term care: the real demographic time bomb

The afternoon workshops on retirement planning and long-term care addressed the issue that is hardest to pin down. According to several speakers, it is not the AHV or the second pillar, but long-term care that is Switzerland’s biggest unresolved funding issue. Today, 85,000 people receive supplemental benefits while living in nursing homes. According to projections, that number will rise to around 140,000 by 2040.

Urs Arbter summed up the crux of the matter: The supplementary benefit, as a government safety net, effectively prevents the emergence of a long-term care insurance market because it eliminates the individual need to make provisions for the future. At the same time, there is no question that this safety net is socially necessary. There is no easy solution.

Lukas Kienast of AXA shared a remarkable finding based on real-world experience: The acceptance of securities-based retirement products can be significantly increased through smarter product design and better advice, without overstretching customers’ risk tolerance. Less talk of guarantees, simpler product architecture, and more understandable language. The share of retirement assets invested in stocks at AXA now stands at 63 percent. Seven years ago, 60 percent of surveyed customers did not want any stocks. Conclusion: Advice works.

From Diagnosis to Implementation

The conference theme set the tone: don’t get bogged down in abstractions, but rather identify levers for change. Three themes ran as a common thread throughout the day: risk transparency and prevention, product design and market development, and demand stimulation and trust.

What remains is a mixed picture. Switzerland is well-positioned compared to other countries in the DACH region, but it is by no means done. Earthquake coverage is lacking, cyber insurance is massively underinsured, and long-term care remains a systemic issue. The industry can and must do more. But it cannot do it alone. The event at the Kunsthaus showed that critical thinking is not only allowed but urgently needed.

Binci Heeb

See also: AI in Pension Planning: An Efficiency Engine with a Sense of Responsibility

Search:

Sponsors: