For a long time, growth was seen as a self-sustaining feature of the modern economy, driven by innovation, productivity and real opportunities. But this logic has been quietly reversed: today, all progress requires more debt, more support and more systemic intervention. The article shows why we are looking at the wrong metrics, how the dynamics have shifted since the 1970s and why governments have a tool that companies do not: They can change the value of money themselves.

For most of modern economic history, growth felt almost inevitable. It was not questioned. It was observed. Capital flowed into factories and railways, not because it had to, but because the opportunities were obvious. Steel production increased, energy became abundant, logistics connected markets that had never interacted before. Productivity did not just improve, it transformed the economic landscape in ways that were visible, measurable, and, above all, intuitive.

Debt existed, of course. It always does. But it followed obediently. It came after the opportunity, not before it. It financed the next expansion rather than propping up the last one. It was a tool, not a condition.

The system moved forward on its own momentum. And because it moved forward so naturally, we came to believe that this momentum was permanent. That it was, in some sense, the default state of the world.

That momentum has quietly reversed.

Not abruptly. Not in a way that would trigger headlines or emergency meetings. But slowly, almost politely, the underlying mechanics have shifted. Growth still registers on the charts. Economies still expand, quarter after quarter. Forecasts are still written, revised, and debated. The language of progress remains intact.

But something deeper has changed. Each increment of growth now requires heavier financial scaffolding. What once emerged organically now needs support. What once accelerated on its own now requires intervention to maintain speed.

The price is rising. The support beams are multiplying. And somewhere beneath the surface, a quiet question begins to take shape:

How long can this continue before the scaffolding becomes the structure itself?

We Have Been Measuring the Wrong Thing

Part of the reason this shift has gone largely unnoticed is that we have been looking at it through the wrong lens. We continue to rely on debt-to-GDP as the central measure of sovereign sustainability. It appears in reports, speeches, and market commentary with almost ritualistic regularity.

But GDP is not income. GDP is everything. It is production in its broadest sense—consumption, investment, government spending, exports. It is an aggregate of activity, not a measure of control.

Debt, however, is not serviced with activity. It is serviced with access. Governments repay their obligations not with what an economy produces, but with what they can extract from it: taxes, social contributions, duties, and other recurring revenues.

This distinction is subtle. But once seen, it is difficult to ignore. A company is not evaluated based on its total sales alone. It is evaluated based on the cash it can use to service its obligations. The equivalent for a country is not GDP. It is sovereign income.

Shift your lens there, and the narrative begins to change, not dramatically, but uncomfortably.

The Slow Drift Becomes Visible

At first, the numbers do not alarm. They move gradually. They adjust. They seem manageable. But when observed over decades rather than quarters, the pattern becomes clearer.

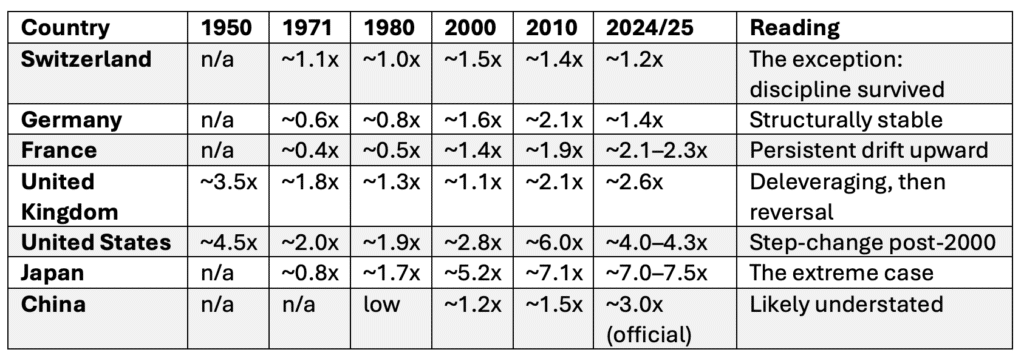

Debt / Sovereign Income (Total Government Revenue)

The movement is not chaotic. It is directional. Debt has pulled steadily ahead of what governments can realistically collect. Not explosively, not dramatically but persistently.

And persistence, in systems like these, matters more than speed. Some countries resisted. Switzerland did so quietly, almost invisibly, without narrative or ambition. Germany, to a degree, followed a similar path contained, measured, cautious.

Others did not. And then there is Japan. Japan does not simply sit at the edge of the system. It operates beyond it. It shows what happens when constraints are not broken, but gradually dissolved. When each postponement of adjustment becomes the justification for the next.

At some point, the numbers cease to function as warnings. They become descriptions of a new equilibrium.

The Moment the System Changed

This evolution did not emerge in isolation. There is a point, subtle in real time, obvious in hindsight, where the trajectory shifts. That point sits in the early 1970s.

In August 1971, the United States closed the gold window. The dollar, until then anchored, however imperfectly, to something external, was released from that constraint. At the time, the move was presented as temporary.

It never reversed. Five years later, the Jamaica Accords formalized what had already become reality: a monetary system no longer tied to a physical anchor, but to policy decisions. From that moment onward, debt did not simply increase.

It became more flexible. And flexibility, while stabilizing in the short term, tends to accumulate consequences over longer horizons.

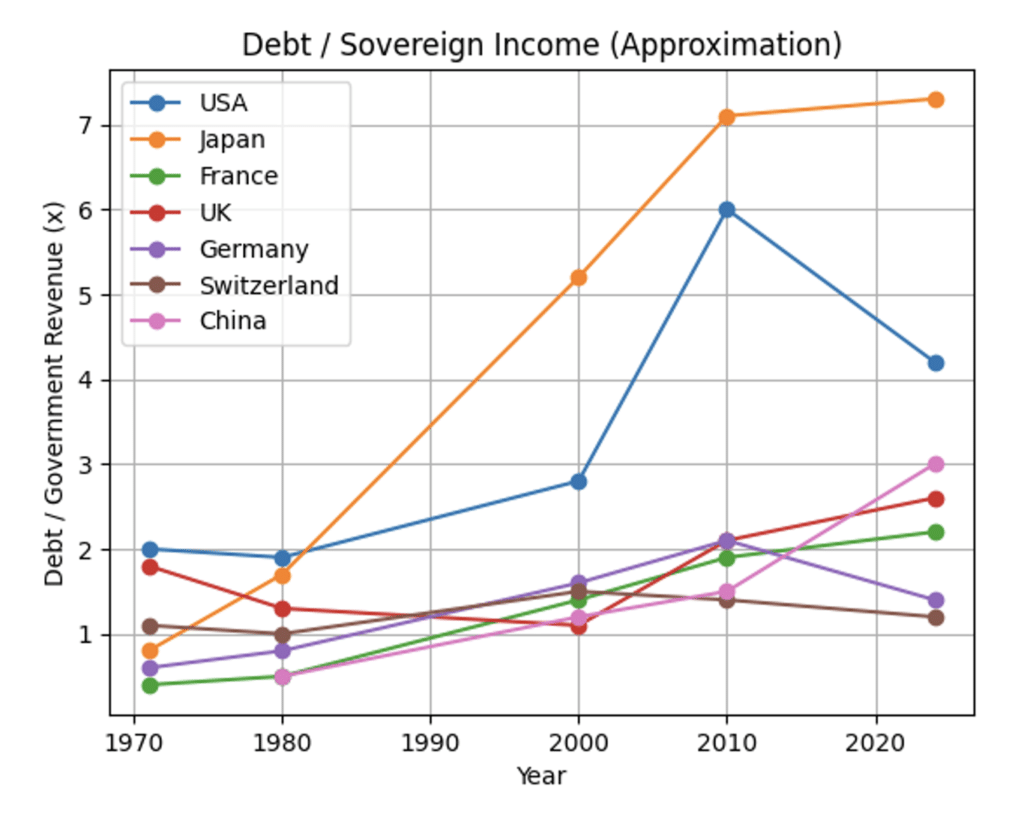

Debt / Sovereign Income (1950–2025)

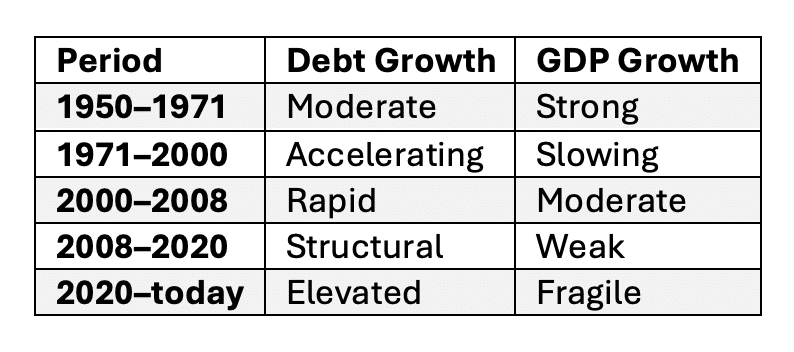

More Debt, Less Growth

What followed was not a collapse. It was something more subtle. Debt continued to grow. Growth continued as well. For a time, the two appeared aligned. But slowly, their relationship changed.

Debt Growth vs GDP Growth

At first, the gap is narrow. Then it widens. Eventually, it defines the system. Debt accelerates. Growth decelerates. And the difference between the two becomes the space where fragility accumulates.

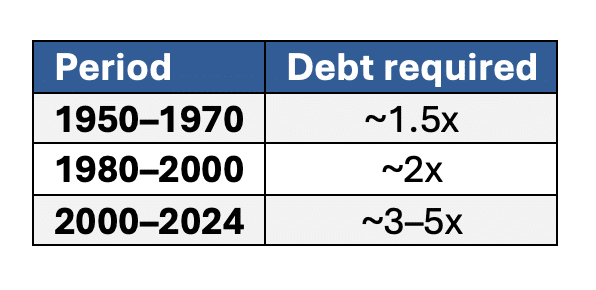

The Price of One Unit of Growth

This leads to a question that is rarely asked directly: Not how much debt exists, but what it achieves.

Marginal Cost of Growth

(Additional debt required for 1 unit of GDP growth)

Each new unit of debt now delivers less real expansion than the one before it. The system still moves. But it no longer moves efficiently. What once amplified growth now compensates for its absence.

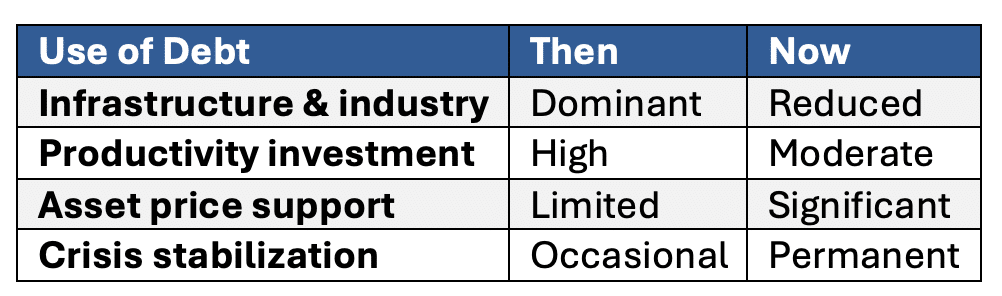

The Purpose Has Changed

And with that, the nature of debt itself has shifted.

Use of Debt Over Time

Debt no longer builds the future. It sustains the present. The scaffolding, once temporary, has become permanent.

Why It Still Holds

And yet, despite all of this, the system continues. No collapse. No definitive break. Because sovereign systems operate under different rules. A company reaches a limit and is forced into resolution. Markets impose discipline. Balance sheets close. A sovereign operates differently. It retains one final instrument. It can change the value of the unit in which its obligations are measured.

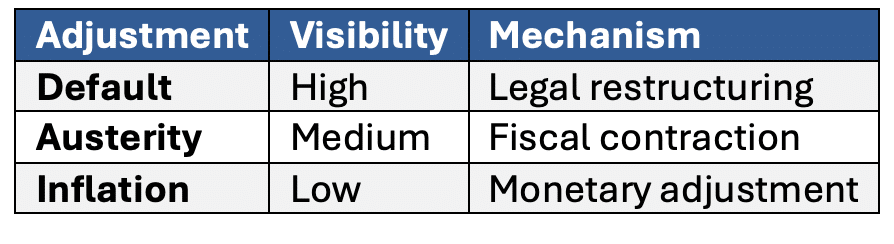

The Adjustment Mechanisms

History is clear on this point. The least visible option is the one most often chosen. Not because it is optimal. But because it is survivable politically, socially, and institutionally.

The Parenthesis

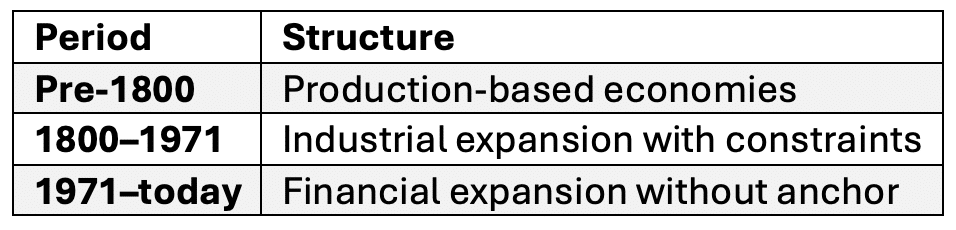

Seen over a longer horizon, the past two centuries take on a different shape. Less a straight line. More a parenthesis. For most of human history, economic gravity lay elsewhere. The West’s rise was extraordinary but not necessarily permanent. It was built not only on industrialization, but on something less visible: The ability to expand debt without immediate consequence.

Economic Structure Over Time

Debt did not accompany this period. It sustained it.

Conclusion

We still tend to think of debt as a temporary deviation, something that builds, peaks, and eventually corrects. But over the past half-century, it has played a different role. It has allowed growth to continue even as its underlying drivers weakened.

And as debt rises faster than income, and as each new unit produces less output, the system does not break in the dramatic way we expect.

It adapts. Slowly. Quietly. Persistently. A company in this position eventually defaults. A sovereign rarely does. It simply changes the value of money. And when that adjustment arrives, it will not be announced. It will simply happen.

Eric Lefebvre

Read also: When Models Fail: The Quiet Death of Economics

Search:

Sponsors: