The global economy seems more complex than ever, but its foundation is surprisingly simple: energy. When energy becomes scarce, expensive or politically uncertain, the entire system comes under pressure. Rising prices coupled with weak growth bring back a word that many economists thought had long been consigned to the history books: stagflation.

Complex systems rarely fail suddenly. As discussed in my column last week, most of the time pressure builds quietly beneath the surface, invisible to most observers. When the explosion finally comes, it rarely creates the problem, it simply reveals it.

Over the past months several questions have returned to economic discussions: inflation that refuses to disappear entirely, geopolitical tensions affecting energy markets, and growing debate about whether the global economy could once again face something many economists believed belonged to the past.

Stagflation.

The first time I encountered that word, I was about fifteen. Until then economics had barely existed in my world. At school nobody really taught it. In many ways that has not changed. Even today surprisingly few people can clearly explain what an economy is.

My curiosity had been triggered a year earlier. In October 1987 global markets collapsed in what became known as Black Monday. I was fourteen.

At that age I could not fully understand what had happened, but the shock stayed with me. Something about the event suggested that markets were not the orderly systems they appeared to be. By the following year curiosity took over. At fifteen I began reading about economics seriously.

What fascinated me immediately was that economics combined everything I enjoyed intellectually: history, mathematics, probability and even a little physics, all applied to something profoundly human.

But the more I read, one question kept returning.

What is an economy?

Economists usually begin with abstractions: GDP, Consumption, Productivity, Interest rates.

But these are outcomes. They describe what happens inside the system, not what the system is.

If we strip the concept down to its physical foundations, the answer becomes surprisingly simple.

An economy is a system that transforms energy into useful things.

Energy becomes motion, motion becomes work and work becomes production.

- Steel is energy transformed.

- Food is energy transformed.

- Transport networks, factories and digital infrastructure all exist because energy has been organised and mobilised.

Without energy nothing happens, no production, no transport, no industry, no economy.

This way of thinking may sound unusual in modern macroeconomic debates, but several thinkers have explored it for decades.

The economist Nicholas Georgescu-Roegen argued as early as the 1970s that economic processes ultimately obey the laws of thermodynamics. The energy scholar Vaclav Smil has documented how every phase of industrial civilisation has been shaped by changes in energy systems. And researchers such as Robert Ayres have shown that improvements in energy efficiency have historically been among the most powerful drivers of productivity growth.

Industrial revolutions, in other words, were not just technological revolutions.

They were energy revolutions.

A simple reality

Strip away the financial jargon and the complex models, and the global economy still rests on something remarkably simple.

Energy.

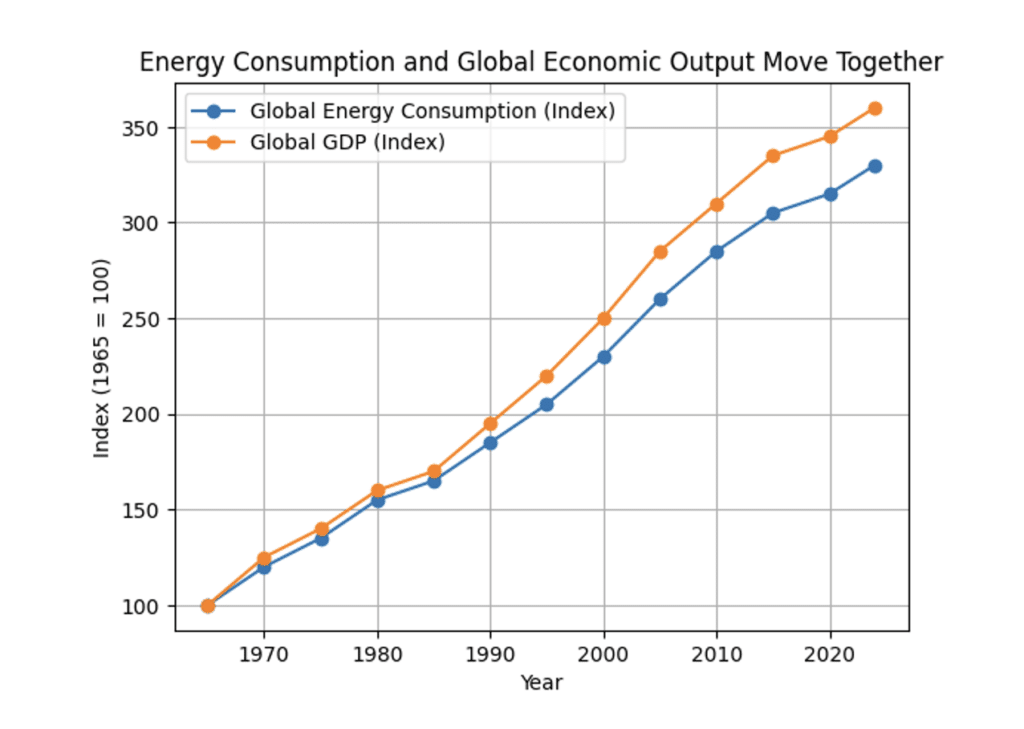

The chart illustrates a striking historical fact: over long periods, global economic output and global energy consumption move almost in parallel. Industrial civilisation, in many ways, is simply an energy system.

Human societies are not an exception to this rule. Nature operates in the same way. Plants transform sunlight into chemical energy. Animals consume calories and convert them into movement, heat and work. Human beings do the same: food becomes energy, energy becomes effort and effort produces results.

For most of history economic activity therefore depended largely on human and animal muscle, occasionally supplemented by wind or water. The discovery and use of fossil fuels changed that equation completely. Coal, oil and natural gas allowed machines to replace human labour by harnessing vast quantities of stored energy accumulated over millions of years.

The scale of this transformation is easy to underestimate. One barrel of oil contains roughly the equivalent of a full year of human labour. Modern transport, industry and logistics therefore operate with millions of “energy workers” embedded in engines and machines performing work on our behalf.

The same logic applies to electricity. A single medium-sized nuclear reactor of around 1 gigawatt produces roughly 8 billion kilowatt-hours of electricity per year, enough to power several million households or large industrial regions.

Industrial civilisation, in that sense, is not only a technological system. It is a system that multiplies human effort through energy.

Finance: organising energy through time

Once energy has been converted into production, societies need mechanisms capable of organising the results of that work across time.

This is where finance appears.

Banks redirect the savings generated by past production toward future production.

Insurers protect the accumulated results of economic activity against unexpected shocks.

In that sense banks and insurers are tools that transform the results of energy consumption and human work into capital that can circulate through time.

Finance sits on top of the real economy.

And when the physical foundation weakens, fragility eventually spreads upward into the financial system.

The paradox that fascinated a teenager

The word that fascinated me, stagflation, combines two ideas: stagnation and inflation.

An economy that stops growing while prices continue to rise. For decades economists believed this combination should not exist. Inflation was supposed to appear when economies overheated, not when they slowed down.

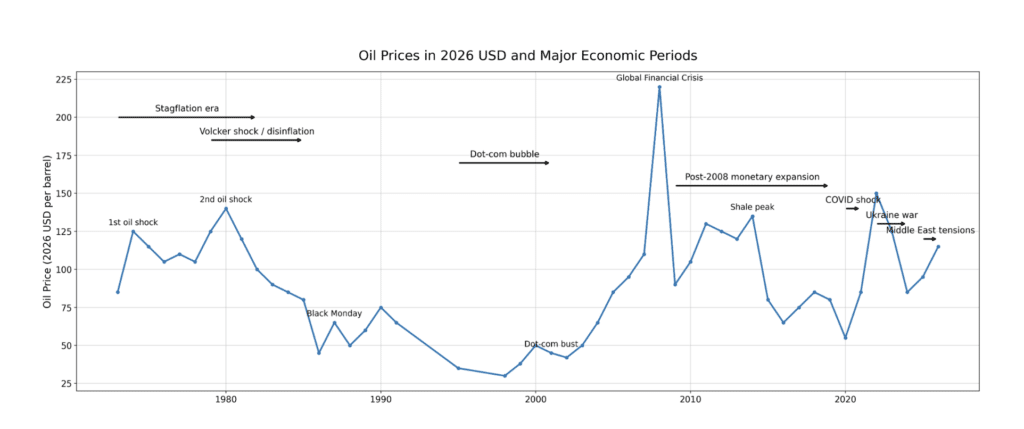

But the 1970s proved otherwise. The collapse of the Bretton Woods monetary system after the Nixon Shock was followed shortly by the 1973 Oil Crisis. Energy prices surged, growth slowed and Inflation accelerated.

Seen through the lens of energy, the paradox becomes easier to understand. When the fuel of the economic system becomes scarce or expensive, production slows while the cost of everything produced rises.

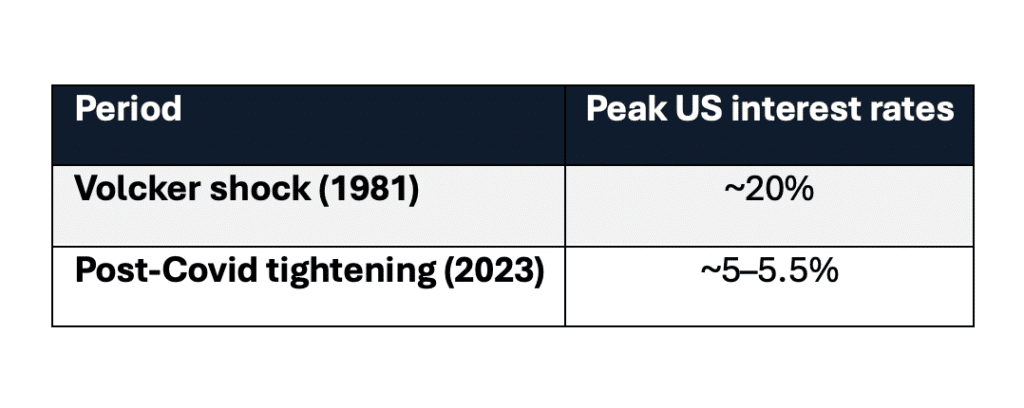

The brutal cure: Volcker’s shock

The stagflationary spiral of the 1970s eventually forced policymakers to confront reality. The cure came in the early 1980s under the leadership of Paul Volcker.

Volcker’s response was simple and brutal: raise interest rates until inflation collapsed.

At one point the Federal Funds Rate exceeded 20%. The medicine worked, but it nearly killed the patient. Two deep recessions followed before inflation was finally crushed.

Volcker vs today

By historical standards the tightening cycle, which followed the COVID years, might almost appear homeopathic compared with the shock therapy applied by Volcker. Which raises a difficult question. If a genuine stagflationary episode returned, would today’s highly indebted global economy survive the same medicine?

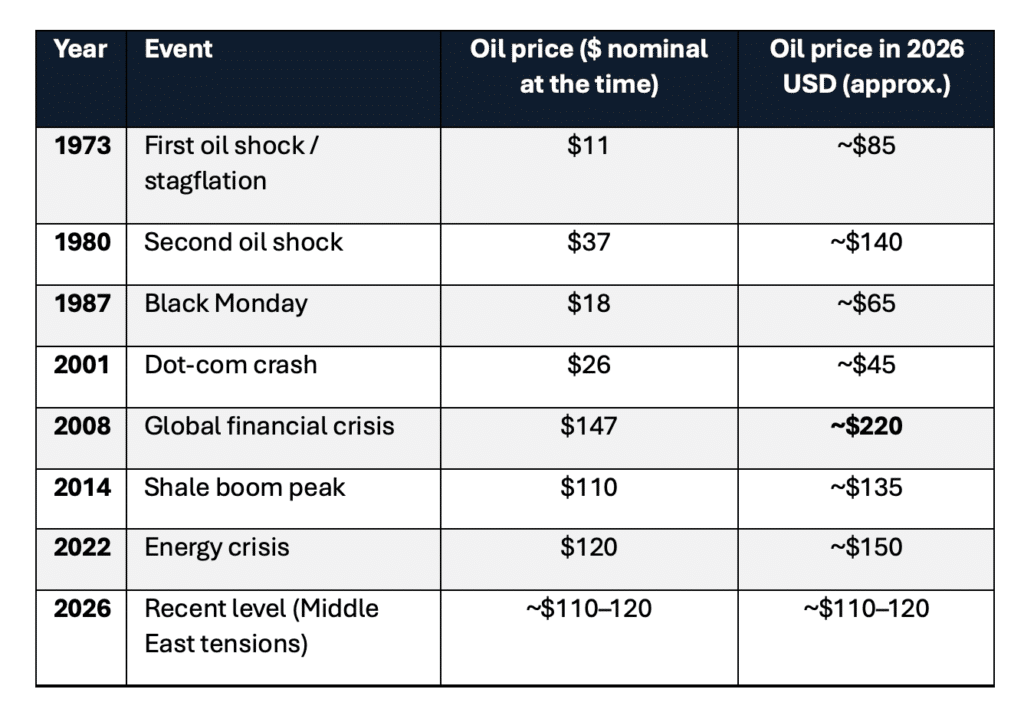

Oil shocks and economic crises

In real terms the 2008 oil spike was larger than the shocks of the 1970s, a fact often forgotten when the financial crisis is discussed.

Energy shocks rarely trigger the explosion, they merely ignite the fuse.

A notable exception: the dotcom crash

Not every crisis follows the same pattern. The collapse of the technology bubble in 2000 was primarily a financial phenomenon. Oil prices remained relatively moderate.

Financial bubbles can burst on their own. But when the energy system itself becomes unstable, the consequences tend to spread far beyond financial markets.

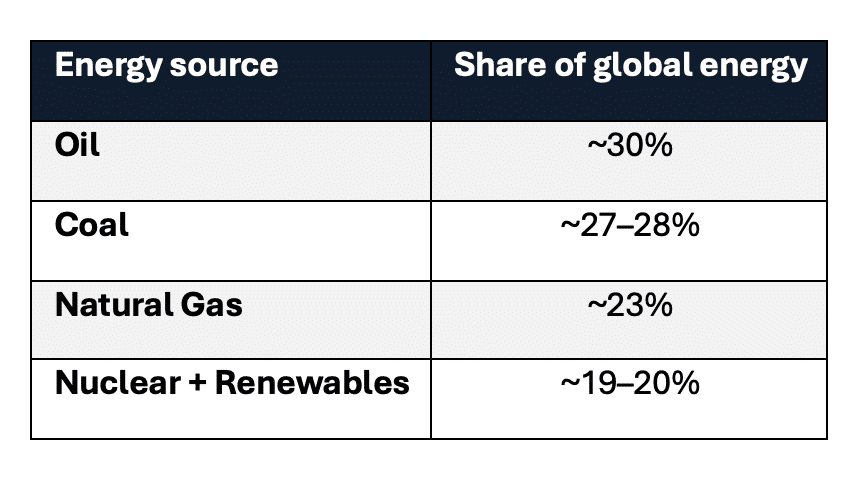

The world still runs on oil

Oil remains the single largest energy source in the world.

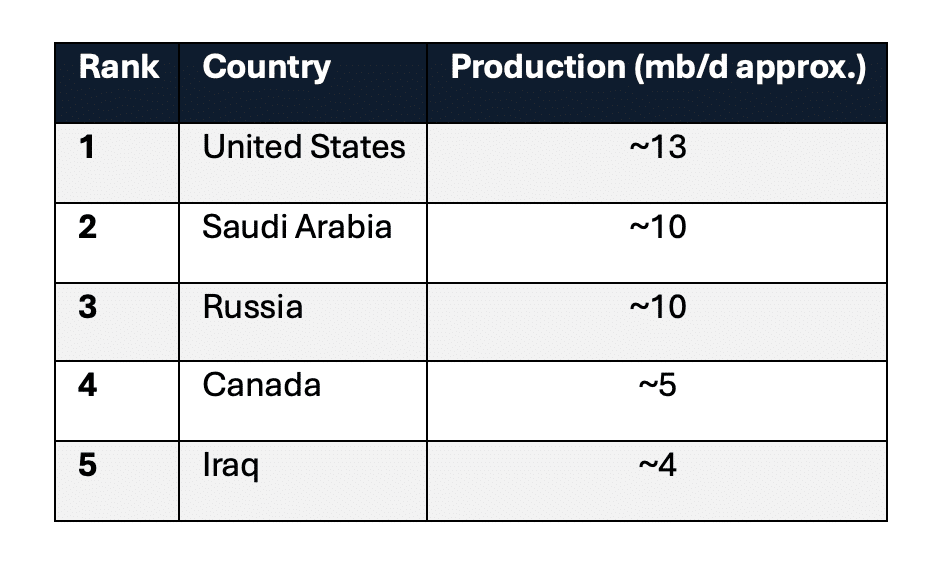

Who produces the most oil?

The United States is today the largest oil producer in the world. Interestingly, the United States was also the largest producer during the 1973 oil shock. History, it seems, swings like a pendulum.

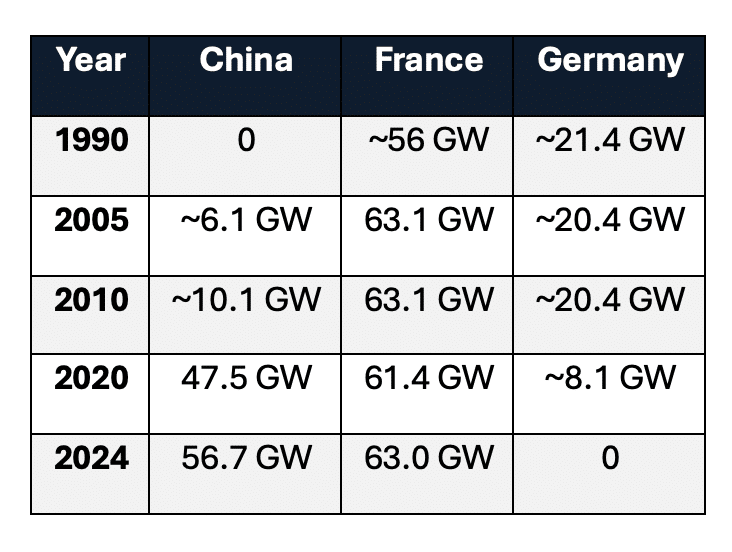

The German energy experiment

Energy policy therefore matters enormously. For decades Germany has been the industrial engine of Europe. German manufacturing, engineering and exports have long been one of the pillars of the European economy. When Germany accelerates, Europe tends to move with it.

Yet over the past decade Germany made a remarkable decision. Following the Fukushima nuclear disaster, Berlin chose to progressively shut down its nuclear power plants, a source of stable, low-cost electricity that had supported German industry for decades.

The contrast with other major economies is striking.

While China expanded nuclear capacity and France maintained its nuclear backbone, Germany dismantled its own. For a time, the consequences remained hidden. Cheap Russian gas replaced the lost nuclear capacity and kept energy prices competitive for German industry. But this model depended on one crucial assumption: that Russian gas would remain cheap and available. When the Russian invasion of Ukraine shattered that assumption, the system suddenly found itself exposed. Sanctions disrupted energy flows. Gas prices surged. Electricity costs rose sharply.

The country that had voluntarily shut down a major source of cheap domestic energy suddenly found itself dangerously exposed to external shocks.

Industrial consequences for Germany

The consequences are now visible across Germany’s industrial base. Energy-intensive sectors such as chemicals, steel and heavy manufacturing have come under increasing pressure.

The chemical giant BASF, one of Europe’s largest industrial energy consumers, has already announced significant restructuring and capacity reductions in Germany.

The automotive sector, long the backbone of German industrial power, is also navigating one of the most challenging transitions in decades as companies such as Volkswagen, BMW and Mercedes-Benz face rising costs and intensifying global competition. For an economy built on manufacturing, energy costs are not a secondary variable.

They are a core competitive factor. Germany represents roughly a quarter of the industrial output of the European Union. When the German engine weakens, the consequences ripple across the continent.

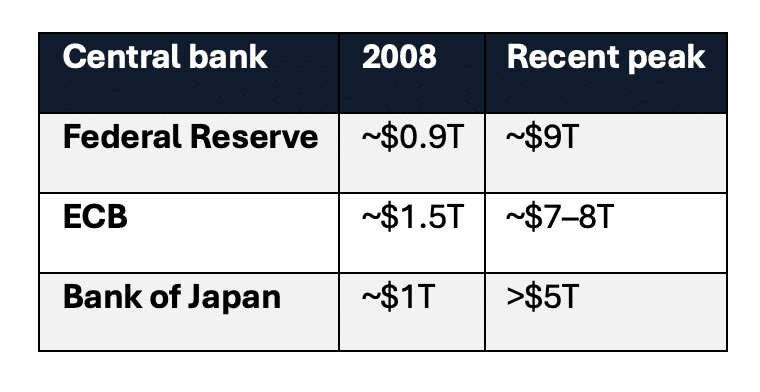

The monetary experiment since 2008

Tens of trillions of dollars of liquidity were injected into the global financial system. Which raises an obvious question. If oil at $147 per barrel destabilised the system in 2008… what would the equivalent shock look like today?

The fuses of the present

Several potential fuses are visible. Geopolitical tensions threaten critical energy routes such as the Strait of Hormuz. Roughly 20 percent of global oil consumption passes through that narrow corridor. None of this guarantees stagflation.

Economies often surprise us. But history suggests that when enough pressure builds beneath complex systems, the smallest spark can release enormous energy.

Beneath the complexity

Financial markets today look extraordinarily sophisticated: Derivatives, leverage, algorithmic trading. Yet beneath all that complexity lies a remarkably simple chain:

energy → work → production → capital

Break the stability of the first link and fragility spreads through the rest of the system. In complex systems the explosion is rarely the surprise. It simply reveals the pressure that had been building all along.

A question for the readers

If economic power ultimately rests on the ability to transform energy into industrial output, which countries are expanding that capability, and which ones are weakening it?

The answer may explain a great deal about the shifting balance of the global economy. We will return to that question.

Because in complex systems explosions rarely appear out of nowhere.

They reveal the pressure that had been building all along.

Eric Lefebvre

Read also: When Troubles Come in Squadrons

Search:

Sponsors: