Concentration, mobility and the modern limits of taxation: the new column shows why income taxes in developed economies rest on a narrower base than is often assumed and why precisely this base is increasingly mobile. A topic that should be approached with caution.

Previous columns in this series have looked at the structures on which modern economies rest: energy as the physical engine of production, credit and bonds as the circulation, debt as the shadow the future casts on the present, and sovereign equity as the long ledger of national stewardship. Each of those columns examined how a piece of the system works.

This week, the focus shifts from how the system runs to what keeps it running. Modern states do not operate on theory. They operate on revenue, on the share of national income claimed each year to maintain the structures the previous columns described. In nearly every developed economy, the most visible and most contested mechanism for that claim is the income tax.

This is a topic where opinions tend to arrive before the facts, and where the facts themselves are often less familiar than the opinions. Some readers will likely disagree with what follows, perhaps strongly. That is fair. The intention here is not to argue a political case but to set out the data as it is published by national tax authorities, and to consider what those numbers imply for the economic system we depend on.

What emerges, when one looks closely, is a structure with two features that rarely receive attention together.

First, the income tax base in most developed economies is far more concentrated than the public debate suggests.

Second, that concentrated base is increasingly mobile.

Together, these features quietly shape what governments can do, and what they cannot.

Who actually pays

Income tax in modern economies is widely described as a system in which everyone contributes. In statistical terms, this is misleading. In every major economy, a large share of total income tax is collected from a small share of taxpayers.

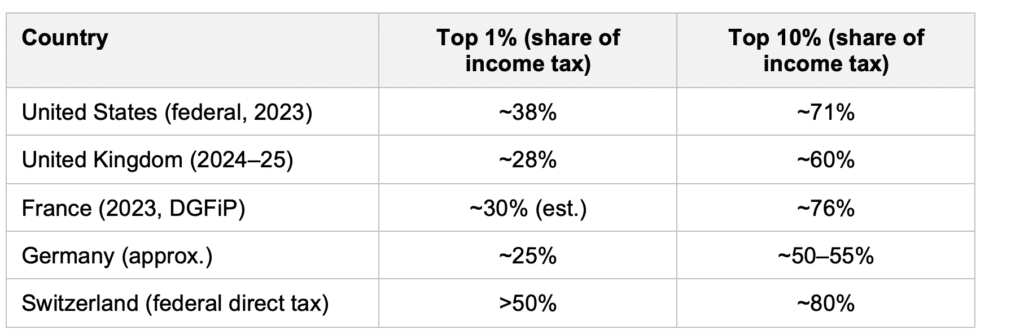

The United States is the clearest example. According to Internal Revenue Service data, the top 1 percent of earners, those with adjusted gross income above roughly 675,000 dollars, paid 38.4 percent of all federal income tax in 2023. The top 10 percent paid 70.5 percent. The top 50 percent paid approximately 97 percent. The bottom half of taxpayers contributed around 3 percent.

The United Kingdom shows a similar pattern. According to HM Revenue and Customs, in 2024 to 2025 the top 1 percent of income tax payers earned 13.3 percent of total income but paid 28.2 percent of all income tax. The top 10 percent earned 35.1 percent of total income and paid 60.2 percent of income tax. Roughly 36 percent of the adult population paid no income tax at all.

France, often perceived as more egalitarian, presents an even more concentrated income tax structure than these two. According to the Direction générale des Finances publiques, the 10 percent of households with the highest incomes contributed approximately 76 percent of net income tax in 2023. Slightly more than half of French fiscal households pay no income tax at all. A useful nuance is that income tax represents only about 7 percent of total taxes and contributions paid by French residents, the rest coming largely from social contributions and value added tax. The income tax itself, however, rests on a remarkably narrow base.

Germany follows a comparable logic, though slightly less concentrated. Switzerland, perhaps surprisingly, sits at the most concentrated end of the spectrum. According to figures from the Federal Tax Administration cited in the KPMG Swiss Tax Report 2025, roughly 80 percent of all direct federal income tax is paid by the top 10 percent of taxpayers. More than half of all federal direct income tax flows from the top 1 percent alone.

These figures use slightly different definitions in each system, and direct cross country comparison should be made with care. But the pattern is consistent. In every developed economy, a small group carries a disproportionate share of the income tax burden. In the United States, the top 1 percent pays more federal income tax than the bottom 90 percent combined. In Switzerland, more than half of all federal direct income tax flows from just 1 percent of taxpayers.

The income tax system is therefore not a flat structure resting evenly across the population. It is a narrow pillar resting on a small base of high earners.

The Swiss laboratory

Among these systems, Switzerland is the most instructive, and in many ways the most distinctive. The country’s overall tax burden stood at roughly 27 percent of GDP in 2024, well below the OECD average of 34 percent. Yet its public finances are not strained, its public services compare favourably with countries that collect significantly more, and the federal budget remains close to balance.

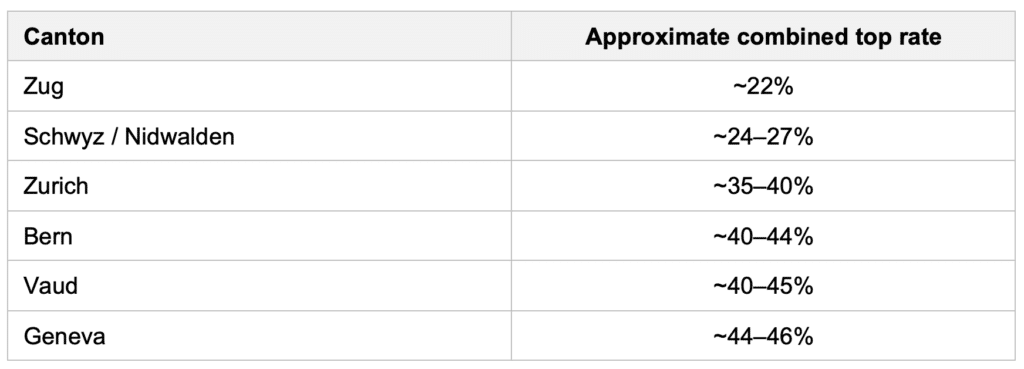

Part of the explanation lies in the federal structure. Income tax is levied at three levels: federal, cantonal and communal. The federal rate is progressive but capped at 11.5 percent, identical across the country. The cantonal and communal rates are not. They vary enormously, by deliberate constitutional design.

A high earner relocating from Geneva to Zug can reduce their effective tax burden by roughly twenty percentage points without leaving the country. This is not a loophole. It is a constitutional feature. The cantons compete openly for residents and corporations, and the federal government has no power to set their rates. The constitution itself imposes a ceiling on federal taxation and requires periodic popular renewal of that authority.

This system has produced two outcomes that are often debated abroad but rarely discussed together. Switzerland collects less tax as a share of its economy than almost any other Western state, yet its tax base is among the most concentrated in the developed world. The discipline imposed by competition, between cantons within Switzerland and between Switzerland and the rest of the world, has shaped both outcomes simultaneously.

When the pillar moves

The concentration of the tax base would matter less if the people who form it were stationary. They are not entirely so.

The historical record contains several instructive episodes.

In 2012, France introduced a top marginal income tax rate of 75 percent on incomes above one million euros. The measure was politically popular at the time and broadly supported in opinion polls. It was abandoned in 2014. Forecast revenue gains did not materialise. Total tax receipts in 2013 came in roughly fourteen billion euros below projection. Manuel Valls, then prime minister, summarised the lesson in a remark that has since entered the language: « trop d’impôt tue l’impôt ». Too much tax kills tax. The seventy five percent rate is no longer law.

France’s earlier wealth tax, the impôt de solidarité sur la fortune, has been studied even more extensively. According to estimates from New World Wealth, approximately 60,000 French millionaires left the country between 2000 and 2017 in association with the ISF and surrounding tax changes. The ISF was largely abolished in 2017 and replaced with a narrower tax on real estate, the IFI.

A more recent and unusually well documented case comes from Norway. In 2022, the Norwegian government raised the wealth tax rate from 0.85 to 1.1 percent and increased dividend taxation. The combined measure was projected to raise an additional 146 million dollars per year. According to research compiled by CitizenX and reported widely in Scandinavian media, individuals representing roughly 54 billion dollars of taxable wealth subsequently relocated, principally to Switzerland. The estimated annual loss in wealth tax revenue alone was 594 million dollars, roughly four times the projected gain. By 2024, more than 300 multimillionaires and billionaires had reportedly left Norway, including the country’s fourth richest individual.

The Norwegian case is illuminating because the tax change was, by international standards, modest. The threshold at which the higher rate applied was relatively low and the increase itself was small. Yet the behavioural response was sharp at the very top of the distribution.

It is important not to overstate this. Recent academic work, and analyses by the Tax Justice Network and others, show that millionaire migration as a share of the relevant population remains small, typically well under 1 percent per year. Most wealthy individuals do not leave when taxes rise. Attachment to family, language, schools, healthcare and accumulated networks anchors most people in place. The French Ministry of the Economy itself reported earlier this year that only about 0.2 percent of the top 1 percent of earners emigrate annually, half the rate of the wider population.

But the income tax base is so concentrated at the very top that even modest flows from the very wealthiest can produce visible effects on revenue. When 1 percent of taxpayers pay between 30 and 50 percent of the income tax, the departure of a few hundred individuals can have a fiscal effect entirely disproportionate to their number. The structural sensitivity is real, even if the typical migration rate is low.

The corporate parallel

A similar dynamic, more visible and longer running, has shaped the taxation of companies.

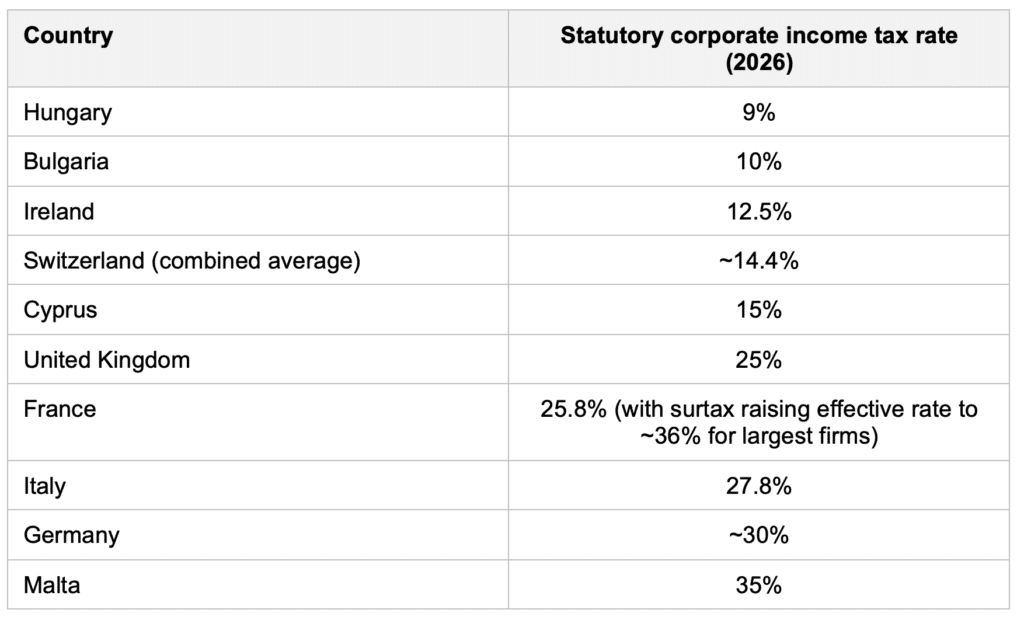

In 1980, the average corporate income tax rate across OECD countries was around 48 percent. Today it is approximately 23 percent. This decline has not been the product of coordinated policy. It has been the product of competition.

For decades, lower rate jurisdictions attracted multinational headquarters, intellectual property and intra-group financing structures. Ireland’s 12.5 percent rate, sustained through several economic cycles, transformed the country into one of Europe’s most important destinations for foreign direct investment. Hungary, with a 9 percent rate, has pursued a similar strategy on a smaller scale. Switzerland’s cantons have been competing among themselves and with the rest of the world throughout this entire period.

This pattern was eventually understood, in many capitals, as a problem. In 2021, more than 130 countries agreed under the auspices of the OECD to introduce a global minimum effective tax rate of 15 percent on the profits of large multinationals, the framework known as Pillar Two. The stated aim, in the OECD’s own language, was to place a floor under tax competition and end the race to the bottom.

Pillar Two has been implemented across most of the European Union, the United Kingdom, Norway, Switzerland and many other jurisdictions since 2024. In January 2026, however, the OECD agreed to a side by side arrangement under which the United States, having declined to adopt Pillar Two formally, would operate its own minimum tax regime in parallel. The framework remains in place. It has not collapsed. But the floor it places under tax competition is partial, and the negotiation around it is ongoing.

The deeper point is that even with a coordinated minimum rate of 15 percent, competition does not disappear. It moves to the design of the base, to subsidies, to incentives for tangible investment, and to substance based carve outs. The Pillar Two rules themselves include a substance based exclusion that allows tax incentives tied to real activity to reduce the effective rate. The contest continues, on different terrain.

A logic familiar to business

There is a way of looking at this that may feel uncomfortable in the context of taxation, but is rarely contested in business. Companies that compete in any open market quickly learn that customers respond to prices, especially when alternatives exist. When sales decline, the question is rarely whether customers have stopped wanting the product. It is more often whether they have found something comparable elsewhere, at a lower price.

Modern states, in a strict economic sense, are also providers. They supply security, the rule of law, infrastructure, courts, education, healthcare, monetary stability and the institutional framework within which production becomes possible. Taxation is the price paid for that bundle of services.

For most of history, this was a price most people had no choice but to accept. The service and the price were tied together by geography. Today, for a meaningful share of high earners and for most large corporations, that is no longer the case. Comparable services are available in other jurisdictions, and the price differs.

When the gap is small, attachment to country, language, family, schools and continuity of life tends to dominate, as the data on actual migration confirms. When the gap becomes large, or when the service is perceived to degrade while the price rises, the calculation shifts. The same logic that nudges a customer toward a cheaper supplier of comparable quality begins to operate. This is an analytical observation, not a normative one. It does not say that taxation is unjust, or that those who leave are right to leave. It simply notes that the logic governing choice in every other domain of economic life does not stop at the door of fiscal policy.

A further observation follows, which is too rarely acknowledged in public debate. The mobility this dynamic implies is not evenly distributed across the income scale. Lower earners are largely tied to where they live, by employment, by family obligations, by language, by the practicalities of moving a household across a border, and often by the absence of any meaningful financial gain from doing so. Higher earners face fewer of these constraints. They tend to have the means, the professional flexibility, the international networks and the legal advice to act on a price comparison if they decide to.

This produces a quiet asymmetry in any tax system designed to extract more from those who earn most. The part of the base most able to respond to price is also the part on which the system most depends. The part of the base least able to respond carries the smaller share of revenue, but the larger share of what cannot be moved.

Two features that fit together

Two features of the modern tax system therefore stand out.

First, the income tax base is highly concentrated at the top of the distribution. In most developed economies, the top decile of taxpayers pays the majority of all income tax collected, and in some, including France and Switzerland, well above seventy percent.

Second, that base is mobile, both for individuals and for corporations. The mobility is not absolute, and it should not be exaggerated. Most people, including most wealthy people, do not move in response to tax changes. But at the margin, where the largest payments come from a small number of decisions, the elasticity is real and visible.

These two features create a quiet trade off that political systems rarely acknowledge openly. Higher rates do not always produce higher revenue. There is a level above which behavioural responses, deferral, restructuring or, in some cases, relocation, begin to offset the intended gains. Where exactly that level lies depends on the country, the design of the tax, the sectors involved and the alternatives available. It is rarely visible until it has been crossed.

The Swiss case shows that this trade off can be managed deliberately. By accepting lower rates and constraining its own ability to raise them, Switzerland has built a system in which a small number of high earners and large companies remain, and pay. The base is concentrated, but it stays.

The French and Norwegian cases illustrate what happens when the trade off is ignored.

A simple conclusion

There is a temptation, in tax debates, to assume that revenue is a function of rates alone. The data does not support this assumption. Revenue is a function of rates and base, and the base, in modern economies, is mobile, at least at the top.

This does not mean that high earners or large companies should be taxed lightly. It means that the question of what they should be taxed cannot be separated from the question of what they will continue to pay if the rate moves. In any other industry, a provider would call this competition. In tax policy, it is too often treated as a betrayal.

Reasonable people disagree about where the right level lies. That is a legitimate political debate, and one this column has no ambition to settle. But the structural reality on which the debate rests, the concentration of the base, the mobility of those who form it, and the asymmetry between those who can move and those who cannot, is not, in itself, contested by the published data of the world’s tax authorities.

A small group pays most of the income tax. That group can move. And when it moves, the loss is not proportional to its size, but to its share of the total. Those who remain, and who carry on paying, are usually those who never had the option to leave.

The pillar is narrower than it appears. And narrow pillars, however solid they look, behave differently when the ground beneath them shifts.

Eric Lefebvre

Read also: The national balance sheet: national wealth, Hartwick’s rule and the responsibility of nations

Search:

Sponsors: